Asian Paints Alchemy 2026

Aviation Industry Report

Market Trends

- The aviation sector in India currently contributes $72 billion to GDP in FY 20

- India has 464 airports and airstrips, of which 125 airports are owned by the Airport Authority of India (AAI). These 125 AAI airports manage close to 78% of domestic passenger traffic and 22% of international passenger traffic.

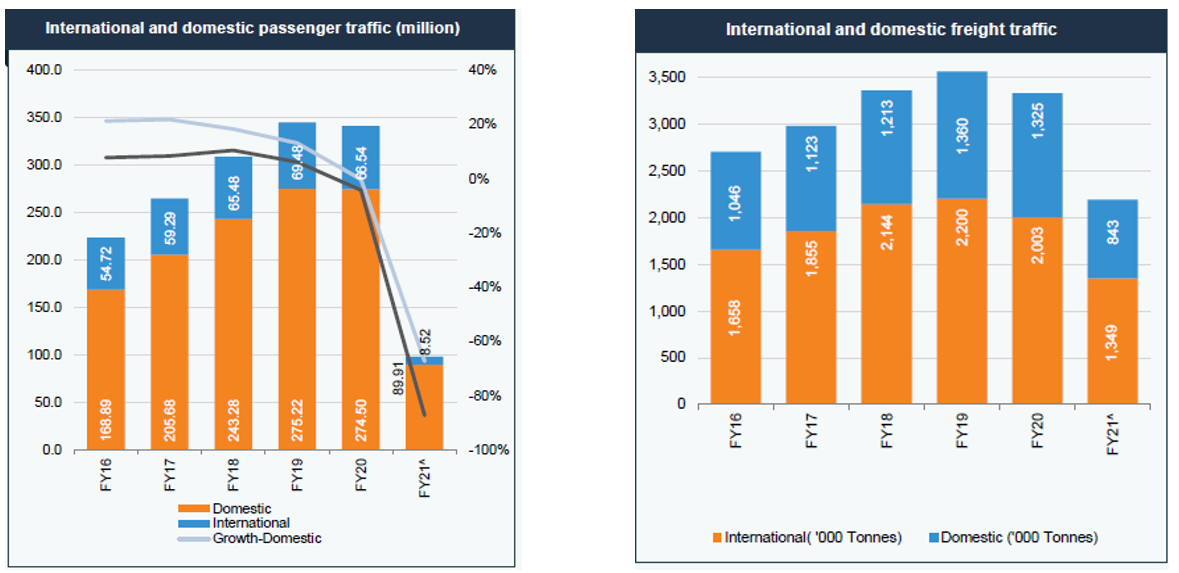

- India’s passenger traffic stood at 98.4 million in FY21, a drastic drop from 341.05 million passengers in FY20, owing to travel restrictions due to Covid 19. Pre-covid, it grew at a compound annual growth rate (CAGR) of 11.13%

- Freight traffic grew at a CAGR of 5.32% during FY16-FY20 from 2.70 million tonnes (MT) to 3.33 MT, but dropped down to 2.19 million tonnes (MT) in FY 21 . Freight Traffic was expected to grow at a CAGR of 7.27% to reach 4.14 MT in FY23.

- India is also the seventh-largest civil aviation market in the world

- Maintenance, Repair & Overhaul (MRO) industry is expected to grow to $1.2 billion by 2020 from $950 million

- To cater to the rising air traffic, the Government of India has been working towards increasing the number of airports. As of 2020, India had 153 operational airports. India has envisaged increasing the number of operational airports to 190-200 by FY40.

- Rising demand in the sector has pushed the number of airplanes operating in the sector. The number of airplanes is expected to reach 1,100 planes by 2027.

- Indian Aviation is expected to surpass the UK and become 3 rd largest aviation market in the world

Major Players

|

Airlines |

Market Share |

|

Indigo |

54.2% |

|

Spicejet |

12.6% |

|

Air India |

11.0% |

|

GoAir |

7.8% |

|

Air Asia India |

6.8% |

Market Size

Passenger and Freight Traffic

Government Policies

1. National Civil Aviation Policy

- VISION: Make flying affordable for the masses; 30 Crore domestic tickets by 2020 & 50 Crore by 2027; 20 Crore international tickets and 10 million tonnes cargo by 2027

- Replace 5/20 with 0/20 rule for international flying rights

- MRO: Develop India as a hub for MRO in Asia; give tax breaks and customs exemptions for it

- Open Sky Policy: For SAARC countries and countries beyond 5000 km; unlimited access to Indian airports; increased flight frequencies with them

- Regional Connectivity Scheme: Price cap on short flights; govt to compensate airlines; levy on metro routes; new airports; concession for airlines

- Safety: Flexibility to DGCA for effective safety oversight and transparent single-window system for issues Air Navigation System: GAGAN satellite navigation system; training centre; robust navigation system Airports: Develop cost-efficient airports with states and PPP; SPV with AAI; high safety standards

2. UDAN- Ude Desh Ka Aam Nagrik

- Duration of 10 years

- Competitive bidding process to select players

Centre provides:-

- Viability Gap Funding

- Concessional GST on tickets

- Code sharing for flights

States provide:-

- GST reduction to 1%

- Facilitate refuelling

- Land for airports

- Subsidized utilities

- 20% of VGF

Airport operators provide:-

- No parking & landing charge

- 42.4% discount on the RNCF

Recent Policy Changes

- 100% FDI in automatic route

- 14 more water aerodromes

- 75% flights allowed to operate post-Nov 2020

- Krishi Udan: help farmers transport agri products

- Lifeline Udan: ferry medical supplies for Covid; Air India

- National Air Cargo Policy

|

Sector |

FDI Cap |

Route |

|

Scheduled Air Transport Service/Domestic Scheduled Passenger Airline in civil aviation |

49% 100% |

Automatic Government |

|

Non-scheduled air transport services in civil aviation |

100% |

Automatic |

|

Helicopter services and seaplanes |

100% |

Automatic |

|

MRO for maintenance and repair organizations |

100% |

Automatic |

|

Flying training institutes; and technical training institutes |

100% |

Automatic |

|

Ground Handling Services subject to security clearance |

100% |

Automatic |

Revenue and Cost

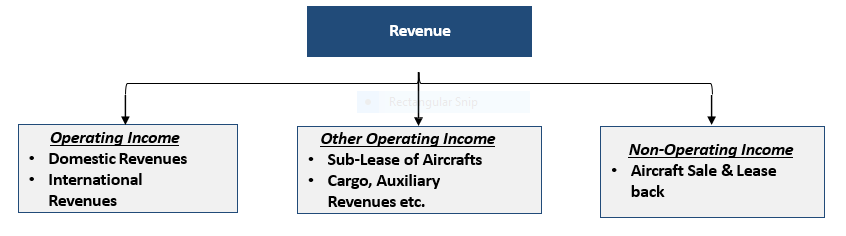

- Domestic revenues are largely INR denominated; Robust pax traffic growth, but yields out of sync with cost structures due to intense competition, government support to a national carrier and customer preference for LCC models

- Airlines with international operations generate part of revenues in foreign currency; foreign carriers

- Dominate in the longer haulage and premium service offerings

- Earnings from aircraft sub-leases (dry or wet) are mostly in $ terms, helps rationalize capacities

- Low contributions from cargo and auxiliary revenue due to their modest adoption level

- With capacity constraints at global aircraft manufacturers & rising commodity prices, market value of successful aircraft models often exceed book values making sale and lease back (conversion of Financial Lease to Operating Lease) an attractive option to book non-operating incomes, generate free cash flows and deleverage the balance sheet

- Most airlines follow an operating lease model for large part of their capacity; Lease rentals are also denominated in foreign currency thereby exposed to fluctuation in forex movement

Cost

- ATF costs contributes 30-45% of overall operating costs for Full Service Carrier’s (FSC’s) & 40-55% for Low-cost carriers (LCCs)

- Domestic ATF prices are linked to fluctuation in

- crude oil prices and movement in INR vs. $

- High central and state levies translates into a 60- 70% higher ATF prices in India over the global average

- Significant congestion at major domestic airports increases fuel costs considerably

- Significant rise in interest expenses due to deterioration in the capital structure, cash losses and increased working capital requirements besides overall rise in interest rates

|

Fuel Cost |

|

Employee Cost |

|

Aircraft Maintenance Expenses |

|

Landing, Navigation & Airport Charges |

|

Selling & Distribution Expenses |

|

General & Administrative Expenses |

|

Other Expenses |

Important Metrics

Low-Cost Carriers (LCC) Strategies\

|

Single model of aircraft |

Reduces maintenance and inventory cost. |

|

Operate on secondary airport |

Lower charges, lower turnaround time due to less congestion |

|

Point to Point Model |

Improves aircraft utilization by reducing waiting time at airports |

|

Single class configuration |

More seats per flight so spread costs over a larger base. |

|

No In-flight services |

Helps to keep the costs and hence the fares low. |

|

Fewer employees per aircraft |

Reduces employee cost and leads to higher employee productivity |

|

E-Ticketing |

Reduces selling expenses per ticket |

|

Ancillary Revenues |

Primarily on-board sales. Provides alternate sources of revenues – helps to reduce break-even PLF. |

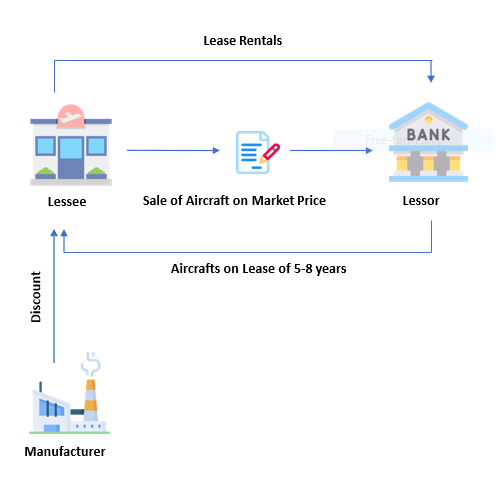

Leasing

Sales and Lease Back Business Model

Benefits of sales and leaseback

- Increased liquidity

- Generation of profits from sale of aircrafts

- Option to purchase the aircrafts at the end of lease term

- Higher flexibility and better efficiency

![]()

Broad Competitive focus

- Air travel was once considered a luxury for both business and private needs. This perception has now changed as savings in travel time, comfort and convenience and higher reliability compared to other modes of travel have outweighed the cost differential.

- The poor connectivity between the metros and smaller cities is why more and more companies and individuals are realizing the benefits of using private jets and helicopters

QCDF analysis of customers preferences in banking industry are given below hierarchically:

- Convenience/Delivery (D) – Convenience along with customer service and trust are the major distinguishing factors in an industry with undifferentiated offerings and services. This along with the tech-based services enables a higher market penetration of users supported by the increasing digital access.

- Personalization/Flexibility(F) –Customer-centric innovation based on personalized services has been recognized as a key aspect of the way forward, by a PwC report.

- Value/Quality (Q) – Airlines confront high competition. The legacy airlines are not only competing among themselves but also with the low-cost airlines. Hence, the carriers have to adapt and improve their service quality. Many view quality as a cornerstone or driving force for improving competitiveness, customer satisfaction and profitability. The quality development is not only to reduce costs and increase productivity but also to better satisfy customers, and improve profitability.

- Cost (C) – Competitions drive the top players to operate at the least cost. But the trust factor and brand value trump best prices for customers. Depending upon the costs various services are provided. The airline industry is divided accordingly into economy class, business class and private planes.

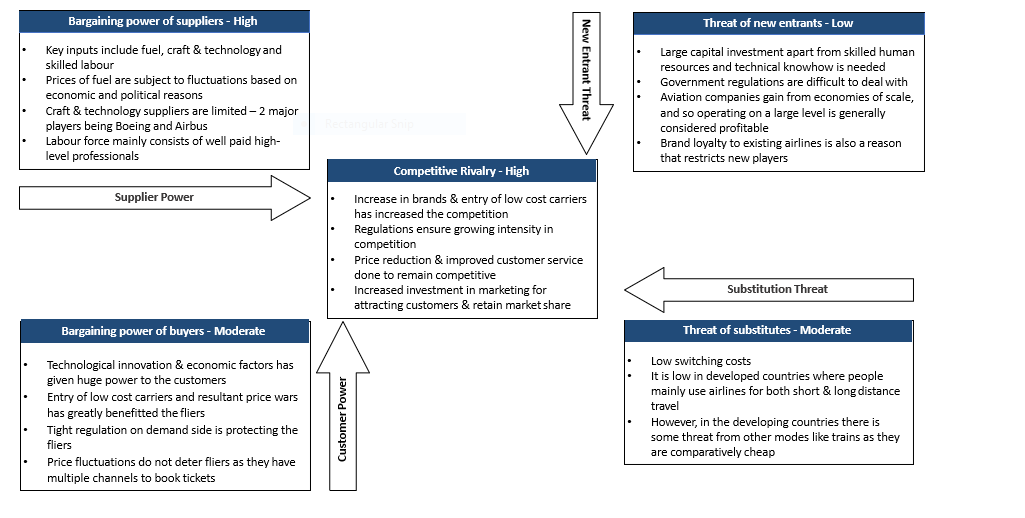

Porter’s Five Forces Analysis

Trends

Technology

- Electric fueled airplane: Built-up organizations like Rolls Royce, Safran and different new companies mean to diminish outflows, flight commotion and expenses, so they have started to create electric impetus frameworks to handle the expanding levels of CO2 discharges identifying with the developing air transport request around the world.

- Urban air versatility: The improvement of UAM, particularly traveller rambles, is relied upon to develop sooner rather than later in corresponding with the need to determine various difficulties identifying with these new methods for transport, for example, new guidelines, new foundation and upgraded traffic the board frameworks.

- Robotized flight decks: This will decrease the requirement for and lead to a related cost-cutting for air bearers. This mechanization improvement is additionally expected to understand the deficiency of pilots, which in the following scarcely any years will turn into an issue for carriers because of the persistent increment of flight activities around the world.

- Digital security: Advanced concepts such as “walk through security” has been introduced to reduce passenger wait times. Biometrics are also used to automate verification process and reduce staffing

- Digital Transformation: Level of digitization is growing quickly and this will lead to connected airport where control center has visibility across all operations and can better monitor and manage performance against key KPI

- Green Airports: High standards have been set to limit noise & air pollution and energy generation from renewable sources. Suppliers such as Siemens and Honeywell have a strong building management service portfolio.

Impact of COVID-19

- Impact on consumer demand – Travel restrictions across the globe, job losses, economic uncertainty and the fear of contracting the virus has drastically reduced the travel demand. As per CAPA there will be ~40-50million domestic travelers and 10 million international travelers in 2020-21 as compared to 140 million & 65 million in 2019-20.

- Impact on supply – Major suppliers like Airbus & Boeing who had manufactured aircraft keeping the demand in mind are facing a conundrum of lower demand and oversupplied markets

- Impact on revenue – AAI reported a 92% fall in revenue from ~2,900 crores during April-June in 2019 to ~240 crores in 2020. Other wings too took a hit, revenue from Indian carriers declined by 86% and airport operators witnessed an 84% drop. Impact on revenue in FY 2021 will be ~50% and job losses including compulsory leave without pay will be ~30%

- Leisure trips to fuel recovery – Leisure trips to visit friends & family will tend to rebound first. Business travel will take longer to recover and even then with remote working and other flexible working arrangements it is expected to reach 80% of pre-pandemic levels by 2024.

- Staggering debt levels will lead to ticket price increases and a larger role for the government in the sector. Many airlines have borrowed huge sums to stay afloat and in order to recoup the costs the airlines will have to increase the ticket prices. Also, when demand for airlines returns it will outpace the supply thereby leading to increased ticket prices

- Greater disparity of performance among airlines – Many airlines have responded to the pandemic by restructuring for greater efficiency. Airlines that are not proactively transforming risk failing to set the business for longer-term structural value creation

- Air freight will see undersupply for some time – Over the past ten years, low cargo rates and the unprofitability of the cargo business have led many airlines to relinquish their dedicated cargo freighter fleets. However, cargo has been a lifeline for the aviation industry during COVID-19.

Reasons for boom in the Aviation Industry

- Foreign Venture Permitted: The legislature declared an arrangement which was de-marked to permit foreign direct ventures of 49% and for NRI completely 100% is permitted to put resources into the residential carrier part. This surely forestalled remote possessed carriers contending in household markets.

- Low Passage Obstructions: The potential outcomes that new firms may enter to influence rivalry. In the Indian avionics division, the boundaries to sections are commonly low prompting various aircraft firing up. However, there are huge hindrances to development and likelihood that exist as administrative confinements, nonavailability of assets after startup as carrier requires a gigantic measure of speculation for the additional turn of events.

- A fascination of outside shores: In order to expand the armada and to diminish the opposition and make the benefit, a portion of the locally worked aircraft grew its tasks abroad. Stream Airways and Sahara have gone global, first to SAARC nations and a while later to SouthEast Asia, the UK, and the US. Following five years of local activity, various local transporters also will be equipped to fly abroad.

- Rising salary levels and segment profile: The interest in air travel is profoundly salaried and flexible. This implies that with the development in the Indian economy, the interest for air ventures is additionally expected to develop.

- Globalization ought to keep on boosting traffic in the long haul. While the world aircraft advertisement is developing at a yearly pace of 4%, the Asian showcase is enrolling 20-30% yearly traffic development in lock-step with the exploding economy.

- The undiscovered capability of India’s travel industry: The advanced countries in the travel industry have just thrived as an aftereffect of mechanical enhancements in airplane plans that have made air travel less expensive.

Difficulties and Challenges for Aviation Sector in India

- Shortage of prepared workers: There is a deficiency of prepared and gifted labour in the avionics segment as a result of which there is merciless rivalry for workers which, in this way, is driving wages to impractical levels. Additionally, the industry can’t hold gifted workers.

- Regional availability: Despite the fact that there is an enormous number of aircraft working, it still needs provincial availability. To expert vide provincial availability is probably the best test going up against the Aviation part in India. The absence of air terminals, likewise hampering the development of provincial availability.

- Rising fuel costs: It is assessed that a proceeding with incremental in-stream fuel cost will represent almost 45% to half of the absolute expenses in 2018. Lately, carriers have taken focal points of fuel supporting projects to balance rising fuel costs, which bolts what’s to come conveyances of fly fuel cost and permits aircraft to confine the vulnerability identified with future costs.

- Declining Yields: Cost or yield is one of the components that is a key factor to aircrafts working benefit or misfortune. Business advancement drove to extreme rivalry and decrease in genuine yields. By the way, the future patterns of yields will be affected by the yearnings of a unique market and its satisfaction by aircraft through the administration of expenses in business sectors that would remain profoundly serious.

- Gaps in infrastructure: Air terminal framework and Air Traffic Control (ATC) establishment are lacking to support improvement while a start has been made to overhaul the framework, the results will be noticeable after certain years.

- High info costs: The info cost is additionally extremely high taking into account a part of the reason like retention charge on intrigue re-installments on remote money credits for airplane securing.

- Technology advancements: With the approach of web and mixed media innovation, there was likewise an apparent danger of business travel being supplanted by video-based meetings calling and webcast business gatherings. Be that as it may, this has not made any huge impact on business travel yet as physical contact is as yet considered for working together.

Recent Developments

- India’s first seaplane service in Ahmedabad started in 2020, which has flights from Ahmedabad’s Sabarmati riverfront to the Statue of Unity

- In 2020, Indigo became the first Indian carrier to operate 1500 flights per day and boast the strength of 250 aircrafts in its fleet

- AAI announced its plan to set up 3 water aerodromes in Andaman and Nicobar islands and 2 in Assam. The government is planning to start a total of 14 more aerodromes across the country

- AAI also announced the construction of a new airport in Arunachal Pradesh and new passenger terminals in Pune, Guwahati and Tiruchirapalli

- Under Union Budget 2021-2022, the government announced a 50% air freight subsidy for agri perishables in North-Eastern states and Himalayan states

- Ministry of Civil Aviation proposed 392 additional air routes under the regional connectivity scheme

- 6 international airports have been completed under the Public-Private partnership initiative of the government

- As of December 2020, 31 Lakh Indian nationals were evacuated and brought back to the country from various parts of the globe under the Vande Bharat Mission. This operation involved 6373 flights from Air India and 474 flights from private carriers in the country. This is one of the largest repatriation missions accomplished by any country in the world

- A significant recovery has been witnessed with passenger traffic and cargo movement quickly rebounding to pre-covid levels. 3,13668 passenger flew on February 28, 2021, which is the highest number since the resumption of domestic flights in May 2020

Future of Aviation in India

Expansion

- With an expansion in the working population and the middle income group in the country, the demand for civil aviation is expected to grow at a higher pace. A rise in domestic and international tourism will also boost the sector. By 2036, India is projected to have 480 million flyers, which will be more than that of Japan and Germany combined.

- By 2023, the total freight traffic is also expected to touch 4.1 million tonnes, growing at a CAGR of 7.27%.

Investment

- The government should take steps towards growth of demand and unlock large investment potential, especially for the private sector and FDI.

- Public-Private partnerships should be encouraged to further develop passenger and cargo aviation in India.

Ancillary Services

- Indian airlines are looking forward to stepping up their ancillary services to ramp up their existing business. This includes services like lounge access, priority boarding, meals and loyalty programs.

Regional Connectivity Scheme (RCS – UDAN)

- Regional connectivity is the key to bring about a boom in Indian aviation. The proposition of new routes and airports, especially in geographies which lack proper rail and road infrastructure, for eg North East India.

India as MRO Hub

- India’s Maintenance, Repair and Operations (MRO) for aviation is expected to grow from $800 million to $2.4 billion by 2028. Airlines will spend 12-15% of their revenues on MRO. This growing demand can be captured from both Indian and international airline carriers.

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment