Asian Paints Alchemy 2026

Banking Industry Report

Market Trends

- The total banking sector assets in 2020 stood around 166 lakh crore rupees, and banking sector assets were around 68.35% as a percentage of GDP, and banking contribution to GDP stood at 7.7%.

- The bank mergers of 2019 brought down 27 public sector banks to 12 in a bid to strengthen the banking sector. The biggest merger was between the Punjab National Bank, Oriental Bank of Commerce, and United Bank that formed the second largest public sector bank.

- Access to the banking system has improved over the years due to persistent effort from the Government to promote banking technology and promote expansion in unbanked and metropolitan regions. The Ministry of Finance launched the Jan Dhan Yojana in 2014, a financial inclusion program to expand affordable access to financial services such as bank accounts, credit, insurance, and pensions in all parts of India. As of 2021, there are a total of 41.6 crore Jan Dhan accounts.

Regulations

|

Regulations |

Purpose |

|

Insolvency and Bankruptcy Code, 2016 |

Provides for a time-bound process to resolve insolvency |

|

Payment and Settlement Systems Act, 2007 |

Provides regulation and supervision of payment methods |

|

Foreign Exchange Management Act, 1999 |

Development and maintenance of foreign exchange market |

|

Banking Regulation Act, 1949 |

Supervision, regulation and licensing of banks |

|

Reserve Bank of India Act, 1934 |

Provides RBI with powers to act as the central bank of India |

Broad Competitive focus

How consumers define their primary bank relationship and how do they find trust with their banking needs? The answers to these questions are seen to be highly influenced by the generation of the user. As per a report by PwC, around 60% of Gen Z open a new bank account through a friend’s recommendation while only 20% of baby boomers follow suit.

QCDF analysis of customers preferences in the banking industry are given below hierarchically:

- Convenience/Delivery (D)– Convenience along with customer service and trust are the major distinguishing factors in an industry with undifferentiated products and services. Quick access to the services at any point from any device is highly sought.

This along with the tech-based services enables a higher market penetration of users supported by the increasing digital access.

- Personalization/Flexibility(F)–Customer-centric innovation based on personalized services has been recognized as a key aspect of the way forward, by a PwC report. This promotes a step back from global banking to a more localized experience.

- Value/Quality (Q) – Capitalizing on the constantly changing technology landscape would differentiate the market leaders. A shift from ownership to influence through regulations changes the role of the government and maintenance of parity among the players, facilitated by the customer perception of the private bankers. The security of the information and the savings are major concerns.

- Cost (C) – Competitions drive the top players to operate at the least cost. But the trust factor and brand value trumps best prices for customers. Wealth management is sought by customers and cross-offerings, with 3rd parties, could be a step in the right direction that reduces costs for the client.

Major Players

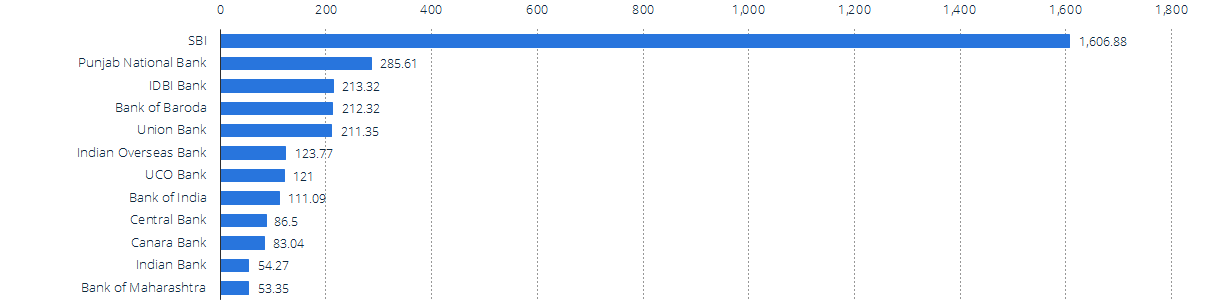

The largest public sector bank of the nation, SBI marks the largest market share with a market capitalization of Rs. 1606 billion.

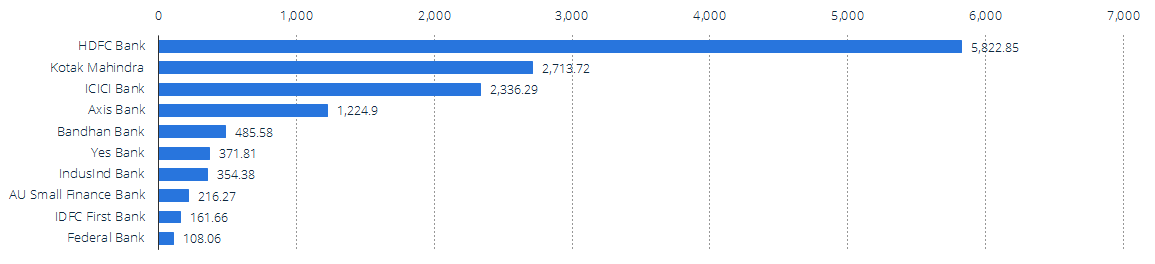

HDFC Bank is the largest bank in the country in terms of market capitalization, with a capitalization value of Rs. 5822 Billion, followed by Kotak Mahindra Bank and ICICI Bank in the private sector.

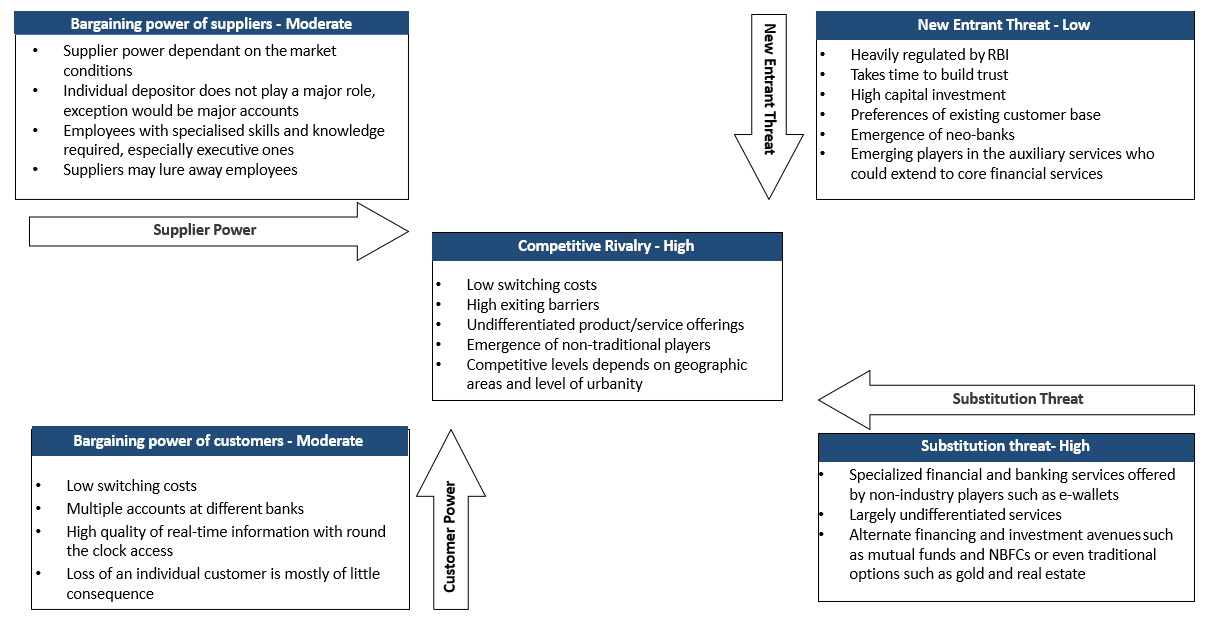

Porter’s Five Forces Analysis

Trends

Technology

- Quantum computing with cloud: A faster and convenient long-term measure to work out complex data operations, ensuring 24x7 access. Extraction of actionable insights from big data and growing them into opportunities would be necessary to maintain a competitive edge.

- Blockchain for risk mitigation and security: The shared infrastructure of blockchain ensures veracity of information, making fraud detection easier. The inherent ease of operation combined with high security, will help decentralize the data and mitigate the threat of cyber attack.

- Neo banks: Virtual banks that operate completely online. They are cheaper, quicker and can leverage a single network with the entire financial portfolio. Being highly customer-centric and with added levels of security, this might be the next big trend to look for.

- RPA and Digital assistants: Robotic Process Automation can be used to deal with low-priority questions and service. Voice interfaces in regional languages can help take digital banking to smaller cities. AI assistants that understand one’s financial capacities and risk tolerance could increase the efficiency of wealth management.

- Cashless economy: Secure instant payments systems that can be used across platforms see a rising trend enabled by third parties such as e-wallets. Increased demand for digital banking with more and more services is seen.

- API platforms: Designed to bridge banks’ backend execution and front-end experiences, provided by banks or third parties. This could help provide low-tech solutions to simple processes.

- Increased no of ATMs: This becomes key to improving customer penetration in Tier III cities and rural areas.

Impact of COVID-19

- The shift towards digital banking was witnessed due to social distancing norms. The decline in branch-driven sales was noticed and was driven by reducing customer walk-ins.

- Negative credit growth because of heightened risk aversion in the banking system created a constraint in financing.

- Reduced demand from SMEs/corporates was a short-term disruption. Non-essential operations were scaled-down and a significant reduction in domestic and cross-border trade was witnessed which led to reduced demand from corporates and small businesses.

- Dip in valuations: COVID-19 has generated significant instability and high volatility in global capital markets. The financial sector has been one of the most affected, with bank valuations dropping in all countries around the world. most banks saw a price slump in mid-March

- Profitability: The low-interest-rate scenario, along with the significant impact of the COVID-19, is reducing the core banking profitability in mature markets. Financial institutions are thus shifting towards commission-based income from the likes of payments and tech businesses.

- Gross NPAs to rise to 14.7% (P) in 2021 from 8.5% in 2020. The option of the moratorium and its extension has aided in the non-recognition (and essentially postponement) of NPAs for the sector.

- Increased credit risk defaults due to business slowdowns and lower recoveries due to moratoriums given to businesses. The borrowers making use of the moratorium facility would be typically more vulnerable relative to others and thus, might reduce future collections as well.

Mobile Banking

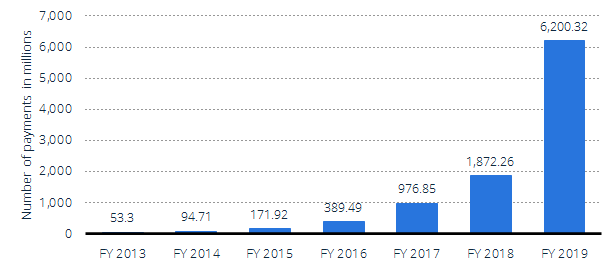

The number of mobile payments witnessed a steep rise in the last 7 years, especially in FY19 where the number of transactions more than tripled as compared to FY20 to reach 6200 million transactions.

Digitization

- By 2022, social media and digital assistants are projected to be primary channels of banking

- In FY 19, India’s digital lending stood at USD 110 billion, and is expected to reach USD 350 billion in the next 5 years

- The government has also been encouraging wide use of wired transaction services like RTGS, NEFT and IMPS. The number of transactions through IMPS increased to 346.5 million and amounted to Rs. 2.88 trillion in January 2021

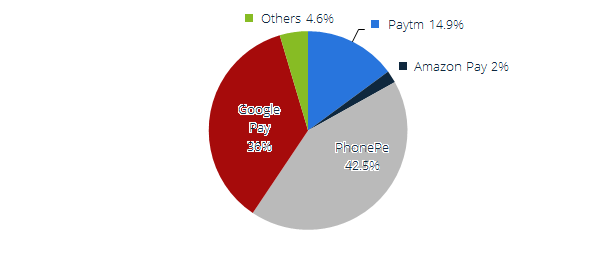

UPI

In February 2021, UPI processed a record number of 2.29 billion transactions worth Rs. 4.25 lakh crore rupees.

Google Pay, PhonePe, and Paytm are the biggest players in the UPI ecosystem.

Rural Penetration

- In 2020, the number of regional rural banks was 43, with the total number of ATMs increased to 209,282

- In a bid to improve accessibility of banking services in rural areas, RBI has allowed regional rural banks with a net worth of minimum Rs. 110 crore to launch their internet banking services

- In 2019, only 48.6% farm households had access to institutional and non-institutional banking services, which is expected to grow with the rapid growth in internet and telebanking across rural India, through mobile banking

Major Players

|

Private Sector Bank |

Market Capitalization |

Details |

|

HDFC Bank Ltd. |

8.55 lakh crore |

Largest Private Sector Bank in India by assets Established in 1994; it has a network of 5,430 branches and 15,292 ATMs across the country |

|

ICICI Bank Ltd. |

4.23 lakh crore |

Established in 1994; it has a network of 5,288 branches, 15,158 ATMs |

|

Kotak Mahindra Bank Ltd. |

3.84 lakh crore |

Established in 2003; it has a network of 1,500+ branches, 2,350+ ATMs covering 744 locations |

|

Axis Bank Ltd. |

2.3 lakh crore |

Established in 1994; it has a large network of 4,528 branches, 12,044 ATMs, and 5,433 cash recyclers spread across the country |

|

Origin Bank |

Number of Branches in India |

Country of Incorporation |

|

Standard Chartered Bank |

100 |

U.S.A. |

|

Citibank |

35 |

U.S.A. |

|

HSBC Ltd. |

26 |

Hong Kong |

|

Deutsche Bank |

17 |

Germany |

|

Barclays Bank Plc. |

17 |

United Kingdom |

|

Public Sector Bank |

Market Capitalization |

Details |

|

State Bank of India |

3.4 lakh crore |

Largest Public Sector Bank in India |

|

Punjab National Bank |

0.40 lakh crore |

Merger of Punjab National Bank, Oriental Bank of Commerce and United Bank |

|

Bank of Baroda |

0.38 lakh crore |

Merger of Bank of Baroda, Vijaya Bank and Dena Bank |

|

Canara Bank |

0.25 lakh crore |

Oldest public sector bank; Merger of Canara Bank and Syndicate Bank |

|

Union Bank of India |

0.22 lakh crore |

Merger of Union Bank, Andhra Bank and Cooperation Bank |

|

Bank of India |

0.21 lakh crore |

One of the founding members of SWIFT |

Road Ahead

Technology

Tele-density or the penetration of mobile phone services has reached 59% in 2020. This could open avenues to mobile banking, which in turn will allow customers to avail banking services from anywhere in the country. Mobile banking is crucial for a country like India as it provides an opportunity to take banking services to a previously untapped market.

Rural Penetration

Rising disposable incomes are expected to enhance the need for banking services in rural areas, and hence drive growth in the banking sector. Government programs like MNREGA have helped improve the income levels of the rural population in the country.

Housing and Personal Finance

Rapid urbanization and growth in disposable income has been encouraging households to improve their standard of living and boost demand for personal credit and housing finance. Credit to the housing sector has increased at a CAGR of 13.4% from FY 16 to FY 20, and is expected to gain further momentum with government schemes like Pradhan Mantri Awas Yojna.

Consolidation

With the entry of foreign banks, the practice of consolidation has intensified and the institutions are increasingly looking at consolidation for enhanced synergies, cost take out from economies of scale and diversification of risks.

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment