ET AI Hackathon 2.0

Cement

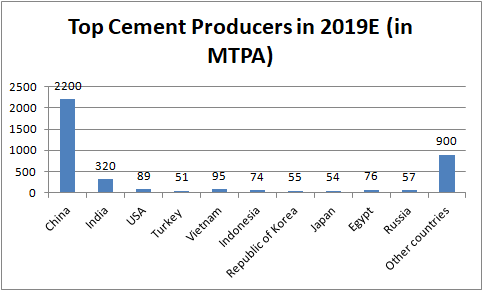

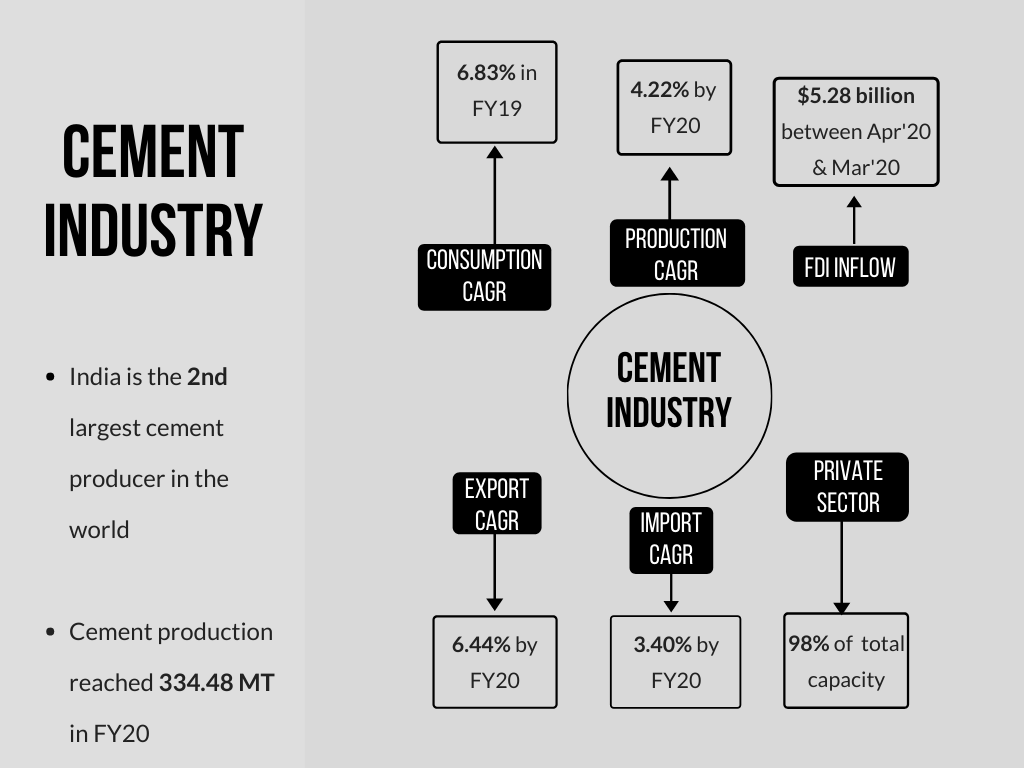

- India is the 2nd largest cement producer in the world. In 2019, it accounted for over 8% of the global installed capacity.

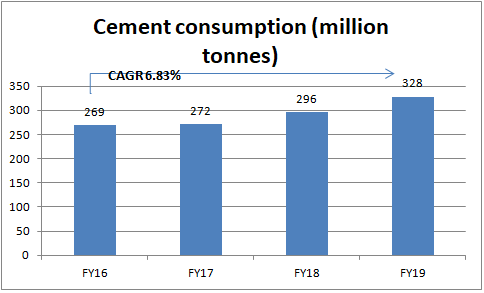

- In FY19, the overall cement production capacity of India was nearly 502 million tonnes (MT) and consumption increased 5%

- The private sector dominates the cement industry with 98% out of the total capacity and the rest with public sector

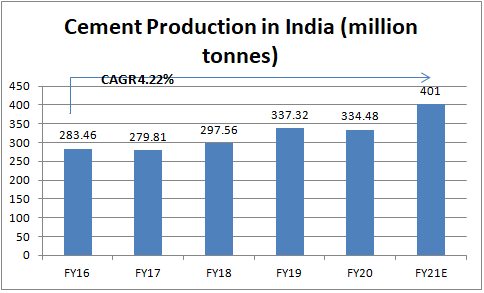

- Cement production reached 334.48 MT in FY20

Competitive Advantage for India

- Long-term cement demand growth rate is estimated at 1.2 times of GDP growth rate

- Northeast, which is witnessing a construction boom, offers attractive investment opportunities

- Oligopoly market, where large players have partial pricing control

- Low threat from substitutes

Government Policies:

- National Infrastructure Pipeline (NIP) introduced projects worth Rs 102 lakh crore (US$ 14.59 billion) for the next five years

- In Union Budget 2019-20, the Government of India extended benefits under Section 80 - IBA of the Income Tax Act till March 31, 2020 to promote affordable housing in India

Investments

- FDI inflow in the industry related to manufacturing of cement and gypsum products reached US$ 5.28 billion between April 2000 and March 2020

Market overview

- Capacity addition of 20 million tonnes per annum (MTPA) is expected during FY19- FY21

- India's cement production is expected to rise between 5-7% in FY20, backed by demands in roads, urban infrastructure, and commercial real estate

- The top 20 companies account for around 70% of the total production

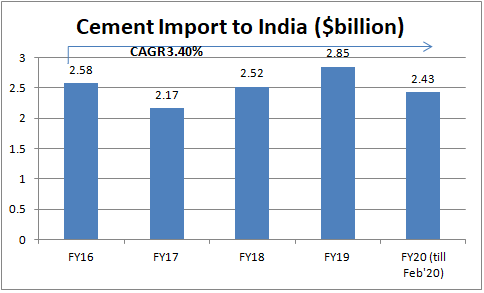

- India’s export of cement, clinker, and asbestos increased at a CAGR of 6.44% between FY16-FY19. In FY20 (till February 2020), it reached US$ 1.83 billion

Strategies updated

- Presence of small & mid-size cement players across regions is increasing, which helps diminish market concentration of industry leaders

- Companies are trying to develop a niche market for Ready Mix Concrete (RMC)

Growth drivers

- India's cement demand was expected to rise 8% in FY20 according to rating agency ICRA

- Public infrastructure projects underway like metro rail projects, dedicated freight corridor, smart cities etc.

- Growth of the industrial sector due to strong economic growth is expected to increase in demand in the long run

- Enhanced interest deduction up to Rs 150,000 (US$ 2,146) for purchase of an affordable house.

New Opportunities

- Per capita cement consumption of cement at 235 kgs is currently the lowest among developing countries as the world averages 520 kgs

- Opportunities available in areas such as housing, dedicated freight corridors, ports and other infrastructure projects

- Northeast, which is witnessing a construction boom, offers attractive investment opportunities

- Strong government’s focus on infrastructure and housing for all by 2022 will lead to high cement demand

Key Industry Organizations

- Shree Cement

- Ambuja Cement

- Ultratech Cement

- Emami Cement

- Ramco Cement

- ACC

- Heidelberg Cement

- JK Cement

- Dalmia Cement

Sources

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment