Asian Paints Alchemy 2026

FinTech industry and open banking API: The two buzzwords every student must know

Let’s first spell out what exactly an open banking API is?

API stands for an application programming interface. In layman’s language, an API is a software that allows two software applications to talk to each other, but with consent. Coming to the next terminology, the formal definition of Open Banking as per Investopedia is, ‘Open banking is a banking practice that provides third-party financial service providers open access to consumer banking, transaction, and other financial data from banks and non-bank financial institutions through the use of APIs. And when it comes to the Indian open baking APIs and the FinTech industry, the performance is sensational!

The booming FinTech industry in India

According to the government agency Invest India, India has the highest FinTech adoption rate globally of 87%, which is much higher than the global average rate of 64%. A joint study conducted by BCG in collaboration with FICCI suggests that with the developments across product innovation, user-experience elation, or deep tech capabilities, India's FinTech industry is expected to become three times as valuable in the next five years, reaching a valuation of USD 140 billion by 2023. This would result in a USD 100 billion value creation opportunity.

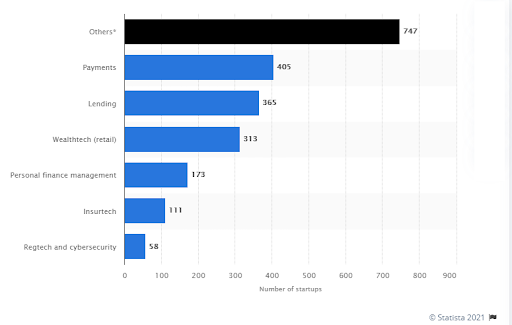

To have a quick look at the Indian Fintech landscape, refer to the chart below which shows the number of startups in each FinTech category in the year 2020:

It can be seen that there were 2174 startups in the year 2020 in the FinTech space, with payment startups as torchbearers. The race to be the next unicorn in the payment space is not surprising given the already set benchmarks by companies such as,

- PayTm: USD16 billion valuation

- CRED: ~ USD 2.2 billion valuation

- Pine Labs: USD 2 billion valuation

- RazorPay: USD 3 billion valuation and many more

Behind all the big numbers, a question arises - what is accelerating this innovation and what is actually going on under the hood?

The how's and why’s of the evolution of the FinTech industry

To understand what is accelerating this innovation and what is actually going on under the hood, let’s go back to 2016 when it all began.

In 2016, the National Payments Council of India (NPCI) launched Unified Payment Interface (UPI) that allowed registered users on applications such as Google Pay, PhonePe, and bank’s in-house developed applications to:

- Access multiple bank accounts from a single platform

- Make transactions online to other banks

This led to an era of Open Banking ecosystem, which allowed customers (retail and others) to transact in a secure, quick, and transparent way using web/mobile apps and banks including small finance, microfinance, NBFCs, etc., regulators such as RBI & SEBI and FinTech companies to build financial products and services that enhance customer experience and satisfy specific customer needs.

But given that not all banks were that technically capable nor had the bandwidth to constantly innovate by launching new products or services, what actually led to the growth of the ecosystem? - Partnerships with fintech companies

Because alone we can do so little; together we can do so much...

FinTech companies have the necessary deep tech capabilities to build and ship products or services at speed & scale. The gold mine that banks were sitting on was customer data. All that was needed now was to connect the bank’s already laid traditional technology infrastructure with newer technical capabilities provided by fintech companies. This connection became possible with two initiatives:

- Open APIs (provided by banks)

- RBI’s regulation that exercises that customers have full control to share their financial data via NBFC account aggregators (link to what are AA)

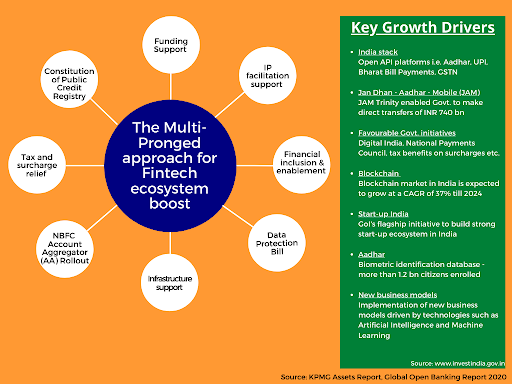

As a result, conceptual entities/business models such as Neobanks, Digital banks, and API aggregators started emerging for real and partnered with well-established banks to build and provide specialized services for customers. In addition to the above two initiatives, a whole gamut of initiatives was taken directed to boost the FinTech industry in the country, as shown below:

Given that banks, private tech companies, government bodies & regulators were involved to establish the foundations of making India into a ‘Cashless Economy’, the market sentiment also gradually started favoring the growth of the FinTech industry.

The ins and outs of an open banking ecosystem

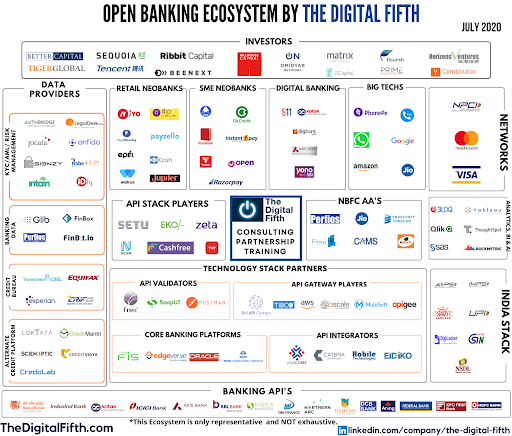

With so many interdependent entities in the open banking ecosystem, how can we visualize the ecosystem in its entirety? So, a management consulting firm DigitFifth structurally organized the whole ecosystem, as shown below, as it appeared in the year 2020.

In order to understand the above chart, start from the bottom and move upwards layer by layer. The bottom layer is the foundational layer formed by the banks and the NBFCs. All the players such as RazorPay, Visa, PhonePe, Oracle, Zeta, etc. above this layer use the secure APIs provided by these banks to provide specialized services to the customers. The products/services offered by these players allow the banks to offer a more personalized experience for their customers given that some of these products are powered by Machine Learning and Artificial Intelligence that enables learning of customer behaviors.

Thus banks are now able to predict the needs of customers and proactively promote only those solutions and offerings that customer needs rather than promoting a one-solution-fits-all kind to every customer. Investors rest on the top of all layers to facilitate the innovations at scale

The future is here: India’s open banking API and FinTech industry

The COVID-19 pandemic has, in fact, led to aggressive innovations in the FinTech industry as banks are now forced towards digitization of almost every banking process to stay in contact with customers and their demands. The new-age companies such as Fi, Signzy, Karza Technologies, CRED, Digit Insurance, Groww, etc. have witnessed positive market reactions from customers and banks alike leading to increased investor confidence in the Indian FinTech space. Private banks such as ICICI, HDFC, YES Bank, and Kotak have launched their open banking platforms in the last 3 to 4 years enabling the FinTech companies access to high-level corporate clients as well as individuals with medium and high income.

Though it is evident that top Private Equity (PE) firms are already pouring large funds to realize the potential of India’s FinTech industry, a report by BCG suggests that in order to fulfill India’s ambition to be a global FinTech hub, India's FinTech sector will need investments of USD 20-25 billion over the next five years.

Another point of consideration is that the industry’s growth depends at large on the tech talent as well, as these professionals will be the ones building solutions on the ground. They are expected to be adept in skills such as AI, ML, Cloud Computing, Blockchain, RPA, Cybersecurity, and the Internet of Things (IoT). Thus, access to a diverse customer base, access to skilled talent, more investor confidence, a robust regulatory framework, and continued participation by various public and private financial institutions as well as NBFCs will ensure that the open banking ecosystem becomes a sustainable business model with the capability to compete and expand to a global scale.

This article was co-authored by Sagar Sangani, in response to D2C Business Sagas. If you'd like to submit your story, click here.

To get more insights into the business world, read:

- The Finshots Story|With 56 lakhs' education loan, do you think you will startup? These young IIM Ahmedabad graduates did!

- How Nina Lekhi built Baggit from a 7k business to a 111 crore venture?

- The TVF story | From being rejected by MTV to giving hits like Aspirants, Kota Factory and Pitchers

- Can you win the startup race without a unique business idea? | Success story of boAt

- Newbie to Numero Uno, Nirma’s story of emerging as the successful underdog

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Blogs you need to hog!

What Innovation Does For Efficiency and Competitiveness in a Corporate Sector?

D2C Admin

Online to Offline Commerce- Everything one needs to know

D2C Admin

How Do You Work Around Branding Guidelines To Be Guidelines And Not Limitations? | Alekhya, Brand Manager- Vivel, ITC | Dove, Unilever

D2C Admin

Data is the new oil! | A talk with BP Biddappa, Executive Director HR, HUL & VP HR, South Asia at Unilever

D2C Admin

Comments

Add comment