Asian Paints Alchemy 2026

Table of content:

- Green Accounting Meaning & Objectives

- Types of Green Accounting and their Examples

- Advantages of Green Accounting over Traditional Methods

- Examples of countries that undertake Green Accounting

- Challenges in Implementing Green Accounting and the Way Forward

Green Accounting: Meaning, Types, Challenges, Benefits [+Examples]

Can economic activity and sustainability go hand-in-hand? Can we quantify and value natural resources and ecosystem services in economic terms? Let's discover.

![Green Accounting: Meaning, Types, Challenges, Benefits [+Examples]](https://d8it4huxumps7.cloudfront.net/bites/wp-content/banners/2023/11/6548c748ac6f5_green_accounting.png?d=1200x800)

Green accounting is a method of measuring and reporting the environmental impact of economic activities. It aims to provide a comprehensive picture of the true costs and benefits of these activities, promoting the integration of environmental factors into decision-making processes. In this article, we will explore the concept of green accounting in detail and understand how, by incorporating such practices, organizations can better comprehend the relationship between economic growth and environmental sustainability.

Looking for a sustainable career option? Register for a 1-on-1 mentorshop session

Green Accounting Meaning & Objectives

Green accounting is a concept that aims to quantify and value natural resources and ecosystem services in economic terms. It helps to capture the impact of economic activities on the environment and incorporates it into traditional accounting methods. By doing so, green accounting provides a framework for assessing the sustainability performance of businesses, industries, or countries.

Green Acconting in Economics

Green accounting in economics integrates ecological concerns into traditional economic measurements, such as GDP. By incorporating costs associated with environmental impacts, green accounting offers a more accurate representation of a nation's economic health and sustainability. It encourages businesses and governments to recognize the long-term benefits of sustainable resource management and environmental conservation, promoting policies that balance economic growth with ecological preservation. This approach aligns economic development with environmental stewardship for a more sustainable future.

Do you know? A study conducted by the World Bank estimated that the value of global ecosystem services is around USD125 trillion per year, which is more than double the global GDP!

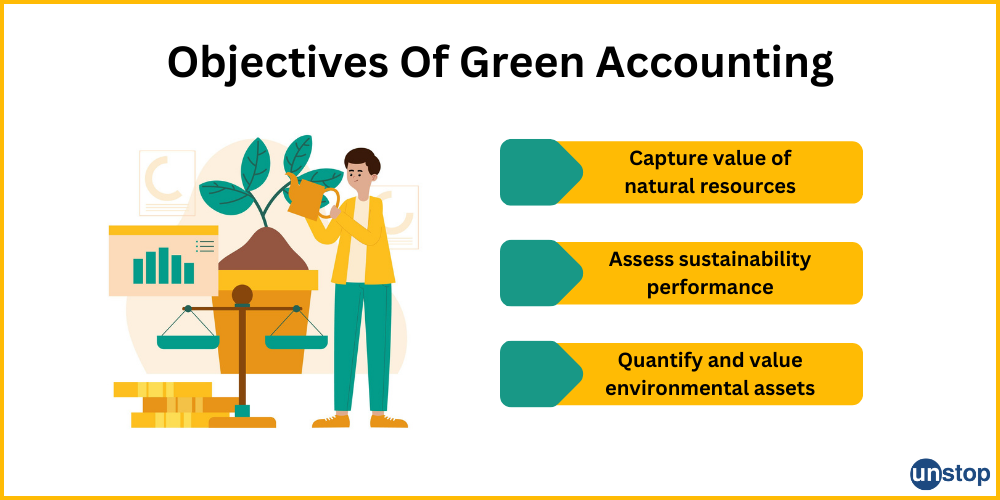

Objectives of Green Accounting

1. Capture the value of natural resources and ecosystem services

One important objective of green accounting is to capture the value of natural resources and ecosystem services. This involves quantifying both tangible assets like forests, water bodies, minerals, etc., as well as intangible assets like clean air, biodiversity, carbon sequestration, etc.

By assigning an economic value to these resources and services, green accounting helps highlight their importance in decision-making processes. The core focus remains on incorporating environment considerations into traditional accounting methods.

2. Quantify and value environmental assets

Green accounting goes beyond traditional financial reporting by incorporating environmental considerations into the valuation process. It involves quantifying and valuing environmental assets such as land use, water resources, energy consumption, waste generation, greenhouse gas emissions, etc. This allows for a comprehensive assessment of the true costs and benefits associated with commercial activities.

3. Assess sustainability performance

Another objective of green accounting is to provide a framework for assessing the sustainability performance of businesses, industries, or countries. Integrating environmental factors into financial reporting systems enables stakeholders to evaluate the negative impact of various entities. This information can be used to identify areas for improvement and make informed decisions regarding resource allocation and management.

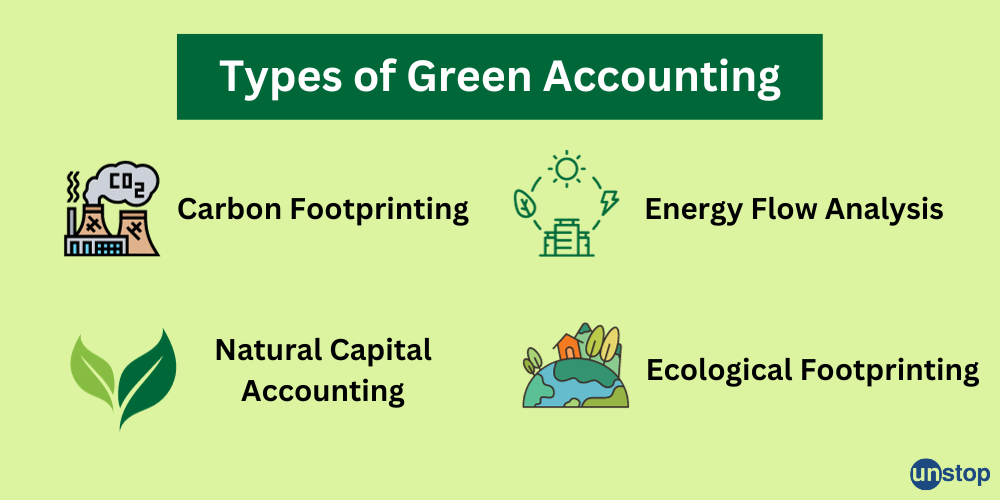

Types of Green Accounting and their Examples

Green accounting encompasses various methodologies that aim to measure and quantify the environmental impact of human activities. Here are some types of green accounting along with examples illustrating their application:

Carbon Footprinting

Carbon footprinting is a widely used method in green accounting that calculates the greenhouse gas emissions associated with a particular activity or entity. It helps organizations identify and understand their carbon emissions, enabling them to develop strategies for reducing their negative impact on the environment.

Example

- A manufacturing company conducts a carbon footprint analysis to assess the emissions generated throughout its production process, from raw material extraction to product distribution.

- An individual calculates their personal carbon footprint by considering factors such as energy consumption, transportation choices, and waste generation.

Natural Capital Accounting

Natural capital accounting involves assessing the value of ecosystems by considering their contribution to human well-being. It goes beyond traditional financial accounting by incorporating ecological services provided by nature into economic decision-making processes.

Example

- A city government values wetlands not only for their aesthetic appeal but also for their role in flood protection. This recognition prompts investments in preserving and restoring wetland areas.

- A company incorporates the value of pollination services provided by bees into its cost-benefit analysis when deciding on land use practices.

Ecological Footprinting

Ecological footprinting means measuring the human demand on nature by estimating the land area required to sustain current consumption patterns. It considers factors such as resource consumption, waste generation, and carbon emissions.

Example

- A country calculates its ecological footprint to determine if it is living within its ecological means or exceeding its biocapacity.

- An organization analyzes its supply chain's ecological footprint to identify areas where improvements can be made in terms of resource efficiency and sustainability.

Energy Flow Analysis

Energy flow analysis focuses on quantifying energy flows within an economy or specific sectors. It provides insights into energy sources, transformations, and end uses, helping identify opportunities for energy conservation and renewable energy adoption.

Example

- A city conducts an energy flow analysis to understand its energy consumption patterns, identify areas of high energy usage, and develop strategies for transitioning to cleaner and more sustainable energy sources.

- An industry sector analyzes the energy flows within its operations to optimize processes, reduce energy waste, and enhance overall efficiency.

By quantifying environmental impacts and valuing ecosystem services, green accounting helps organizations and policymakers make informed choices that balance economic growth with environmental stewardship.

Advantages of Green Accounting over Traditional Methods

Green accounting, also known as environmental accounting or sustainable accounting, offers several advantages over traditional methods. By considering externalities that are often ignored in conventional approaches, green accounting provides a more comprehensive understanding of the true costs and benefits associated with business activities.

Considers Externalities Ignored in Traditional Methods

One significant advantage of green accounting is its ability to consider externalities that are typically overlooked in traditional methods. Externalities refer to the costs or benefits that are not reflected in market prices. For example, pollution costs resulting from industrial activities are often borne by society at large rather than the businesses responsible for them. Green accounting takes these externalities into account, allowing for a more accurate assessment of the overall impact on the environment and society.

Enables Better Decision-Making

By incorporating environmental costs and impacts, green accounting facilitates better decision-making processes. It provides valuable information about the long-term consequences on natural resources and ecosystems. This enables policymakers, businesses, and individuals to make informed choices that prioritize sustainability and resource efficiency. With this knowledge, stakeholders can evaluate alternative options and select those that minimize harm to the environment while maximizing social welfare.

Promotes Sustainable Practices and Resource Efficiency

Another advantage of green accounting is its promotion of sustainable practices and resource efficiency. By including environmental costs in financial statements or reports, it raises awareness about the importance of conserving natural resources. This encourages businesses to adopt environmentally friendly practices such as reducing waste generation, implementing energy-efficient technologies, or investing in renewable energy sources.

Identifies Potential Risks and Opportunities

Green accounting helps identify potential risks and opportunities related to environmental factors for businesses or economies. By analyzing data on resource consumption, emissions, or waste generation over time, it highlights areas where improvements can be made or where risks may arise. For example, a company that heavily relies on fossil fuels may face financial risks due to increasing carbon pricing or stricter environmental regulations. Green accounting allows organizations to proactively identify such risks and take appropriate measures to mitigate them, ensuring long-term sustainability.

Terms you must know

What is NNP? Net National Product (NNP) is a measure that adjusts Gross National Product (GNP) by deducting the depreciation of natural resources caused by commercial activities. This adjustment takes into account both the positive contributions from economic growth and the negative impacts on the environment. By incorporating sustainability considerations into national accounts, NNP provides a more accurate measure of economic progress.

What is GGEI? Global Green Economy Index (GGEI) is a ranking system that evaluates countries based on their performance in the green economy. It assesses various indicators such as leadership and climate change, efficiency sectors, carbon markets, and sustainable tourism. By analyzing these factors, the GGEI provides valuable insights into the correlation between a country's green economic performance and its overall sustainability efforts.

What is SEEA? SEEA stands for System of Environmental-Economic Accounting. It is an internationally recognized framework that integrates environmental and economic data to provide a comprehensive assessment of the mutual relationships between the economy and the environment. The SEEA helps policymakers and analysts make informed decisions by providing a standardized approach to measuring and valuing environmental resources and their contribution to the economy.

What is Social Accounting? Social accounting is a framework that integrates social and economic data to understand the relationship between the economy and society, aiding decision-making by valuing social contributions.

Examples of countries that undertake Green Accounting

Norway, China, and New Zealand are some examples of countries that have taken significant steps towards implementing green accounting practices. These nations recognize the importance of incorporating environmental factors into their economic systems to promote sustainable development.

Norway: The Norwegian System of Environmental-Economic Accounts (NSEE)

Norway is renowned for its comprehensive approach to green accounting. The country has established the Norwegian System of Environmental-Economic Accounts (NSEE), which aims to integrate environmental data into national accounts. This initiative allows policymakers and economists to assess the impact of business activities on the environment and make informed decisions regarding sustainable development strategies. By valuing natural resources and ecosystem services, Norway ensures that economic growth aligns with environmental preservation.

China: Incorporating Environmental Factors into National Accounting

China acknowledges the significance of sustainable development and has made strides in incorporating environmental factors into its national accounting system. The country recognizes that traditional measures like Gross Domestic Product (GDP) do not adequately capture the true costs associated with resource depletion or pollution. As a result, China has introduced initiatives such as "green GDP" calculations that account for environmental degradation caused by human activities. By considering both economic growth and ecological sustainability, China aims to achieve a more balanced approach to development.

New Zealand: Natural Capital Accounting Framework

New Zealand has developed a Natural Capital Accounting (NCA) framework to assess the value and condition of its natural resources. This approach recognizes that natural capital, including forests, waterways, and biodiversity, plays a crucial role in supporting commercial activities and human well-being. The NCA framework quantifies the benefits derived from these resources and monitors their condition over time. By integrating this information into decision-making processes, New Zealand aims to ensure that its economic growth is sustainable and does not compromise the country's natural heritage.

Green Accounting in India

In India, green accounting has gained significant attention in recent years due to the country's growing awareness about environmental degradation and the need for sustainable development. The government has recognized the importance of valuing natural resources and incorporating their economic value into decision-making processes for social well-being.

One of the key initiatives in green accounting in India is the implementation of the System of Environmental-Economic Accounting (SEEA). SEEA is a framework developed by the United Nations that provides guidelines for integrating environmental and economic data. India has been actively working towards adopting SEEA and incorporating it into its national accounting systems.

Challenges in Implementing Green Accounting and the Way Forward

The implementation of green accounting poses several challenges that need to be addressed for its successful integration into economic frameworks. These challenges include data availability, valuation methods, and political will.

Data Availability

One of the primary concerns in implementing Green Accounting is the availability of accurate and reliable data. To accurately measure the impact of economic activities, comprehensive information on resource consumption, pollution levels, and ecosystem services is required. However, gathering such data can be a complex task due to various factors, including limited resources, lack of standardized methodologies, and difficulties in obtaining data from diverse sectors.

Valuation Methods

Valuing ecosystem services accurately is another significant challenge in implementing green accounting. Ecosystem services refer to the benefits that humans derive from nature, such as clean air, water purification, carbon sequestration, and biodiversity conservation. However, assigning a monetary value to these intangible services is complex due to their diverse stakeholder perspectives and inherent difficulty in quantifying their worth. Different valuation methods exist, but selecting an appropriate approach that considers social preferences while capturing ecological significance remains a challenge.

Political Will

Political will plays a crucial role in implementing green accounting. It requires governments to prioritize environmental sustainability alongside economic growth. However, there may be resistance from certain interest groups or industries that perceive green accounting as a threat to their profitability or competitiveness.

How to address the challenges?

Here are some ways that can be effective to overcome the above challenges:

- Standardized methodologies can be developed for collecting data on resource consumption, pollution levels, and ecosystem services.

- Best policy and practices can be shared among countries to improve data collection systems.

- Valuation techniques can be refined through collective efforts and deliberations.

- Awareness among the population about the importance of green accounting can be raised, encouraging more countries to embrace this approach.

- Overcoming resistance requires strong leadership and effective communication about the long-term benefits of incorporating environmental considerations into economic decision-making.

To sum up, green accounting is important in achieving sustainable development by providing a comprehensive framework to measure and manage the negative effects on the environment. It enables organizations and governments to account for the costs and benefits associated with commercial activities, ensuring that economic development is achieved while minimizing environmental harm. By incorporating environmental factors into accounting practices, decision-makers can make informed choices that balance economic prosperity with ecological responsibility. Afterall, it is all about securing our present and preserving the future.

Suggested Reads:

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment