ET AI Hackathon 2.0

Table of content:

- Long-Term Investment Meaning

- Factors to Consider Before Long-Term Investment

- Risks of Long-Term Investment

- Advantages of Long-Term Investment

- Who Should Invest for Long Term?

- Conclusion

- Frequently Asked Questions

Long-Term Investments: Types, Risks, Benefits

Explore various long-term investment options, factors to consider before investing, associated risks, and key advantages to help you make informed financial decisions.

Imagine planting a tree. In its early days, it may seem small and unimpressive, but with time, care, and patience, it grows into a towering presence, providing shade and fruit for years to come. Long-term investment works the same way. It requires commitment, strategic planning, and a long horizon to reap substantial financial rewards.

Unlike short-term trading, which focuses on quick gains, long-term investing is about stability, wealth accumulation, and financial security. You may be saving for retirement, a child’s education, or financial independence, but choosing the right investment avenues can make a world of difference.

This article explores various long-term investment options, factors to consider before investing, associated risks, and key advantages to help you make informed financial decisions.

Long-Term Investment Meaning

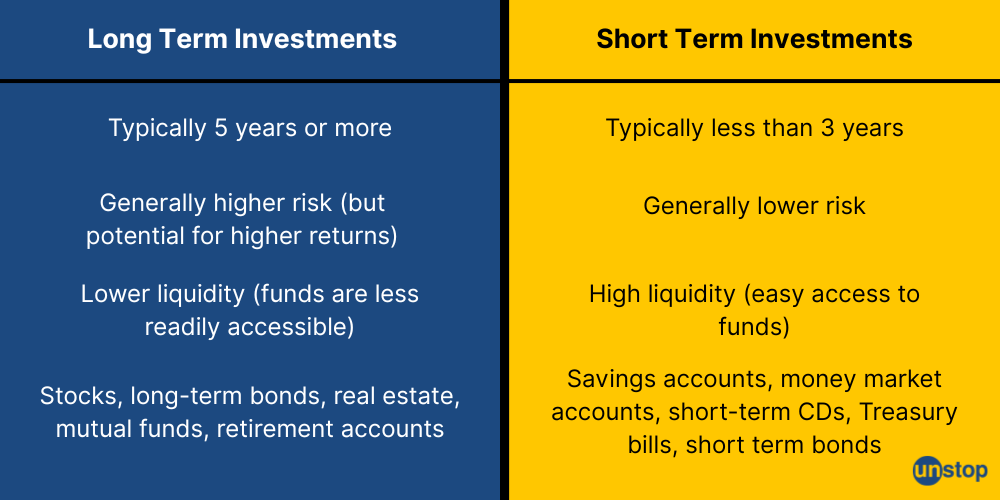

Long-term investment refers to the practice of allocating funds into financial assets or real estate with the intention of holding them for an extended period, usually five years or more. The goal is to achieve capital appreciation, generate passive income, and benefit from compound interest, which helps build substantial wealth over time.

Where to Invest

Long-term investments can be made in various asset classes, including:

-

Stocks: Investing in shares of publicly traded companies allows individuals to become partial owners of businesses. Over time, stock prices tend to increase as companies grow and generate profits. Stocks also offer dividends, providing an additional income stream. While they carry market risks, they have historically provided higher returns compared to other investment options.

-

Mutual Funds: These are professionally managed investment pools that collect money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. Mutual funds help mitigate risks through diversification and are ideal for investors who lack the expertise to manage individual stocks. They can be actively or passively managed, with the latter tracking an index such as the NIFTY 50.

-

Real Estate: Investing in properties, whether residential or commercial, can generate rental income and long-term appreciation. Real estate is a tangible asset that offers stability and serves as a hedge against inflation. However, it requires significant capital, ongoing maintenance, and is relatively illiquid compared to other investments.

-

Gold & Precious Metals: Precious metals like gold and silver have been traditional stores of value and a hedge against inflation. They tend to perform well during economic downturns and periods of currency depreciation. Gold can be invested in physical form (jewelry, coins, bars) or through financial instruments such as gold ETFs and sovereign gold bonds.

-

Bonds: Bonds are fixed-income securities issued by governments, corporations, or municipalities. Investors receive regular interest payments and get back the principal amount upon maturity. Bonds are considered lower-risk investments compared to stocks, but their returns are usually moderate. Government bonds, in particular, are highly secure and suitable for conservative investors.

-

Fixed Deposits (FDs) & Recurring Deposits (RDs): FDs and RDs are bank deposit schemes offering guaranteed returns over a fixed period. FDs provide a lump sum return at maturity, whereas RDs involve regular monthly deposits. These are risk-free investments ideal for conservative investors looking for stable income. However, returns may not always beat inflation.

-

Exchange-Traded Funds (ETFs): ETFs are investment funds that trade on stock exchanges like individual stocks. They contain a mix of assets such as stocks, bonds, or commodities, providing diversification at a low cost. ETFs are passively managed and track indices, making them a good option for investors seeking broad market exposure without active management.

-

Retirement Funds: These include provident funds, pension plans, and annuities designed for long-term financial security. Contributions to retirement funds often provide tax benefits and ensure financial stability post-retirement. Employees can invest in schemes like the Employees' Provident Fund (EPF) or the National Pension System (NPS) to build a retirement corpus.

Factors to Consider Before Long-Term Investment

Before committing to long-term investments, consider the following factors:

-

Investment Goals: Define your financial objectives, such as wealth accumulation, retirement planning, or education funding. Your investment choices should align with these goals.

-

Risk Tolerance: Assess your ability to handle financial losses. Some investments, like stocks, are riskier but offer higher returns, whereas bonds and FDs provide stability with lower returns.

-

Time Horizon: Consider how long you can stay invested. Longer time horizons allow investments to recover from market fluctuations and benefit from compounding.

-

Market Trends: Analyze the past performance of investment options and evaluate their future growth potential based on economic conditions and industry trends.

-

Diversification: Reducing risk by spreading investments across multiple asset classes ensures that poor performance in one area does not heavily impact your overall portfolio.

-

Liquidity Needs: Determine how easily you can access your funds if needed. Real estate and retirement funds have lower liquidity, while stocks and mutual funds are more accessible.

-

Inflation Impact: Ensure your investments generate returns that outpace inflation to maintain purchasing power over time.

-

Tax Implications: Understand the tax benefits and liabilities associated with each investment. Some investments offer tax exemptions, while others may be subject to capital gains tax.

Risks of Long-Term Investment

While long-term investments provide the potential for wealth accumulation, they also carry inherent risks that investors must consider:

1. Market Volatility

Stock markets and mutual funds are subject to price fluctuations due to factors such as economic conditions, geopolitical events, and investor sentiment. While long-term investors can ride out short-term dips, extreme volatility can still impact portfolio performance, especially if funds are needed during a downturn.

2. Economic Downturns

Recessions, financial crises, and unexpected economic disruptions (such as pandemics) can significantly reduce investment returns. Economic slowdowns can cause stock prices to fall, real estate values to decline, and interest rates to fluctuate, all of which can negatively impact long-term investments.

3. Inflation Risk

Inflation erodes the purchasing power of money over time. If an investment’s returns do not exceed inflation rates, the real value of wealth declines. For example, if inflation is 6% and a fixed deposit earns only 5%, the investor effectively loses purchasing power despite earning nominal returns.

4. Interest Rate Fluctuations

Changes in interest rates directly affect fixed-income investments like bonds and fixed deposits. When interest rates rise, bond prices typically fall, leading to lower market value for existing bonds. Conversely, falling interest rates can reduce earnings on new fixed-income investments, affecting long-term portfolio performance.

5. Company-Specific Risks

Investments in individual stocks or corporate bonds are subject to risks specific to the company, such as poor management decisions, declining profitability, or industry disruptions. A company’s bankruptcy or regulatory issues can lead to significant financial losses. Diversification can help mitigate this risk, but it cannot eliminate it completely.

6. Liquidity Issues

Certain long-term investments, such as real estate, private equity, and some bonds, are not easily converted into cash when needed. Selling these assets can take time and may require accepting lower-than-expected prices, making it difficult to access funds for emergencies or other financial needs.

Advantages of Long-Term Investment

Despite the risks, long-term investments offer significant benefits, making them an essential strategy for wealth creation and financial stability.

1. Compounding Growth

Compounding allows investors to earn returns on both their initial investment and previously earned returns. Over time, this effect accelerates wealth growth. For example, an investment of INR 1 lakh growing at 10% annually will become INR 2.59 lakh in 10 years and INR 6.72 lakh in 20 years due to compounding.

2. Resilience to Market Fluctuations

Short-term market fluctuations can cause panic selling, leading to losses. However, long-term investments tend to recover from downturns. Historical trends show that despite periodic crashes, stock markets generally trend upward over the long run, rewarding patient investors.

3. Tax Benefits

Many investment options offer tax advantages that can enhance returns. For instance, contributions to retirement funds (such as NPS in India) provide tax deductions, and long-term capital gains on equity investments enjoy lower tax rates compared to short-term gains. Certain bonds and fixed deposits also offer tax exemptions under various government schemes.

4. Financial Security and Wealth Accumulation

Long-term investing helps build substantial financial reserves, ensuring a comfortable lifestyle, funding major life goals, and securing retirement. A well-planned long-term portfolio reduces dependency on active income and provides financial stability.

5. Lower Transaction Costs

Frequent buying and selling of investments incur brokerage fees, taxes, and other transaction costs. Long-term investing minimizes these expenses by reducing the number of trades, allowing more of the investment’s value to compound over time.

Who Should Invest for Long Term?

Long-term investments are suitable for individuals and investors with specific financial goals and risk tolerance:

1. Young Professionals

Starting early gives young professionals a crucial advantage—time. The longer the investment horizon, the greater the impact of compounding. Even small, consistent contributions can result in significant wealth over decades. For example, investing INR 5,000 per month at an annual return of 12% can grow to nearly INR 1.5 crore in 30 years.

2. Retirement Planners

Those planning for retirement benefit from long-term investments as they help accumulate a substantial retirement corpus. Investing in pension funds, mutual funds, or diversified portfolios ensures financial security and a steady post-retirement income.

3. Parents Saving for Children’s Future

Parents looking to fund their children’s education, marriage, or other future expenses should consider long-term investment avenues such as education savings plans, mutual funds, or fixed deposits to ensure they have the required funds when needed.

4. Risk-Tolerant Investors

Individuals comfortable with market fluctuations and volatility can invest in high-growth assets like stocks, mutual funds, and real estate. While these investments may experience short-term swings, they often yield high returns in the long run.

5. Wealth Builders

Those aiming for financial independence and wealth accumulation benefit from a disciplined, long-term investment approach. By consistently investing in a diversified portfolio, they can achieve financial freedom and passive income generation.

Conclusion

Long-term investment is a strategic approach to wealth creation and financial security. By carefully selecting assets, diversifying, and considering key factors like risk tolerance and time horizon, investors can achieve significant returns. While risks exist, they can be managed with informed decision-making and a well-structured portfolio.

Quiz Time!!!

Frequently Asked Questions

Q1. How long is considered a long-term investment?

Long-term investments are typically made for five years or more.

Q2. Are long-term investments risk-free?

No, they involve risks like market volatility and inflation impact, but diversification helps mitigate them.

Q3. Which is the safest long-term investment?

Fixed deposits, government bonds, and gold are considered relatively safe options.

Q4. Can I withdraw money from a long-term investment early?

Yes, but it may lead to penalties, lower returns, or financial losses.

Q5. How can I start investing for the long term?

Identify goals, research investment options, and consult a financial advisor if needed before making decisions.

Suggested Reads:

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment