Asian Paints Alchemy 2026

Table of content:

- Important Bank Interview Question and Answers (2026)

- Piece of advice for facing bank interview questions

30 Important Bank Interview Questions And Answers (2026)

If you're looking for a job in the banking sector, then race ahead of the competition by practicing the commonly asked interview questions listed here. Also, find sample answers.

Banking sector jobs are one of the most sought-after jobs in the country. So if someone has advised you to look for a job in the banking sector, consider it good career advice. This is because the banking industry is one of the fastest-growing sectors, has fixed working hours, and offers decent salaries and job stability.

Seeing the prospects of banking jobs, this sector has candidates with educational qualifications from varied fields such as finance, engineering, marketing, law, and so on. Normally in the hiring process for banking jobs, written exams are conducted to recruit candidates for different banking posts. After clearing the written exam stages, the selected candidates are interviewed to understand their awareness of the banking sector.

Topics such as types of banking policies, financial assets, tax regime, money supply, Indian economic conditions, stock market, and banking-related current affairs are always on the list of banking interview questions. So if you are one of the candidates aspiring to be a banking professional, a quick review of the commonly asked questions could take you a step closer to your dream. Here are some important bank interview questions and answers for you.

Important Bank Interview Question and Answers (2026)

So what do they actually ask in a banking job interview? Below are some bank interview questions that will give you a good overview of the different types of bank job interview questions that are commonly asked.

Q1. Why do you want to join the banking sector?

This is one of the common interview questions. Hence, you must be well-prepared to answer it. Refrain from saying that banking offers a stable career right at the start. You can begin by telling the interview panel that you are seeking to work in a field that has both challenges and growth and banking offers both of these. Since this job requires both attitude and aptitude, you consider yourself a good fit for the sector. You can also say that banking professionals are considered to be well-organized, logical, and good communicators who are excellent in customer service skills and have strong leadership skills and well as analytical mindset. So because you possess all these qualities, this would be a good career option for you.

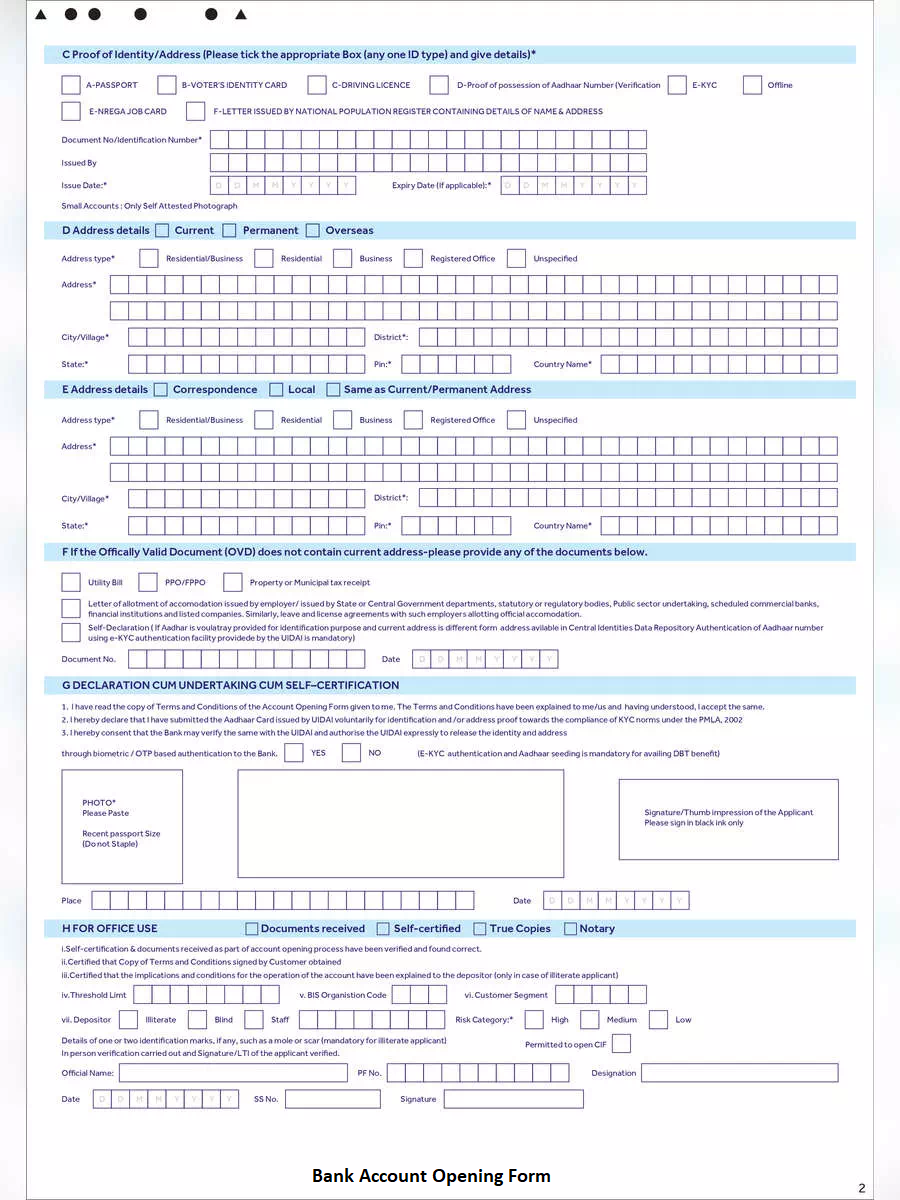

Q2. Can you tell us what documents are required to open a bank account?

If you are opting for a banking career, you must be aware of such basic procedures. Going by the RBI instructions which is the central bank of India, banks have to follow the Know Your Customer (KYC) guidelines. This means that the bank has to obtain some personal information of the account holder. For this purpose, the important documents required would be identity proof like a PAN card, Aadhar card, etc., address proof as well as photographs of the person who intends to open the bank account.

Q3. Why is KYC important?

KYC stands for 'know your customer' and has been made mandatory by RBI since 2004. It is done to make sure that the banks are not being used to carry out illegitimate activities such as money laundering. Another reason is that with KYC, banks can determine the legal status of an entity by cross-checking the operating address and verifying the identities of the authorized signatories. Without KYC one cannot open a bank account or carry out cash transfers or any financial transactions.

Q4. What are commercial banks?

These types of definition-based questions are common bank interview questions. For this particular bank interview question, you can say that a commercial bank refers to any financial institution that is involved in accepting deposits, granting loans, and offering basic financial services such as savings accounts and certificates of deposit to businesses. Its customer base includes large corporates and small and medium enterprises. It is thus different from a retail bank (also called a consumer bank) because a retail bank provides these services to individuals. Commercial banks make money through interest earned from providing bank loans while deposits from bank customers provide commercial banks with the capital to make the loans.

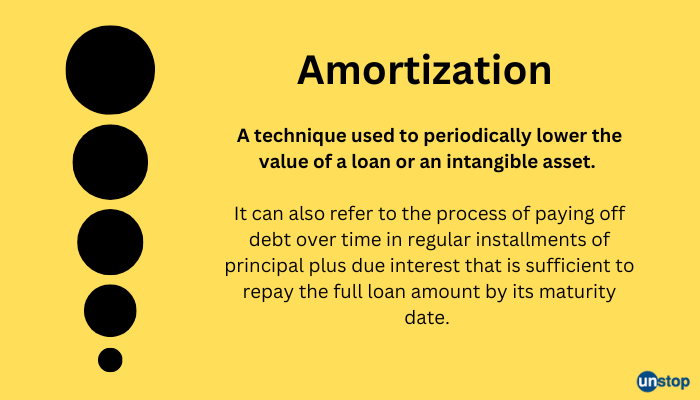

Q5. What is amortization?

You must be aware of the technical terms related to banking. The answer to this bank interview question is that amortization is the repayment of a loan by installment to cover the principal amount with interest.

Note: Negative amortization happens when the loan repayment amount is less than the accumulated interest.

Q6. Can you tell us how do banks earn profits?

This bank interview question intends to understand your basic knowledge of the banking system. You can start by saying that a bank can earn profit in various ways such as by accepting deposits, giving personal loans on interest, through charges on services such as ATM banking, advisory services, investment management, etc. So banks basically give lower interest rates on deposits and charge higher interest rates on loans which fetches them profits apart from other customer services.

Q7. Define debt to income ratio.

Debt to income ratio or DTI ratio refers to the percentage of the gross monthly income that is spent in paying the monthly debt payments. It is used by lenders to determine the borrowing risk. Debt to income ratio is calculated by dividing the total monthly debt payment of a loan applicant by the monthly gross income. Borrowers with low DTI ratios are expected to manage their monthly debt payments effectively. As a result, banks desire a low DTI ratio before issuing loans to any potential borrower.

Q8. What do you mean by the line of credit?

If you read the newspaper regularly, you may have often come across this term, especially in relation to one nation extending the line of credit to some other friendly country. As per its definition, a line of credit or LOC is an agreement made between the bank and the borrower, to provide a certain amount of loans on the borrower’s demand. The advantage of this arrangement is that borrower can withdraw the desired amount (not exceeding the maximum limit or credit limit) at any moment and pay the interest only on the amount withdrawn and not the entire loan payment. Thus, it provides flexibility to the borrower who can adjust the repayment amounts as per the needs or cash flow.

Q9. Who is authorized to print money in India?

The Reserve Bank of India (RBI) prints currency in India and manages it. On the other hand, the Government of India regulates what denominations to circulate in the economy. Hence, Indian government is independently responsible for minting coins.

Q10. Tell us about the different types of bank accounts.

You must have a good idea about the types of accounts in banks that they provide to serve different needs. following are the types of bank accounts:

- Saving Account: These types of bank accounts are most common in Indian banks. Using these accounts, consumers keep their saved money safe for the future. In lieu of the deposit made and to incentivize the customers, banks provide a certain percentage of interest on the savings in these bank accounts. Hence, your money grows over time. This account type is used by the customers to best keep their money to be used in case of emergencies safe. The good thing is that anyone can open a savings account in a bank including children. However, their account is operated by a parent or guardian till they attain the age of 18 years. A minimum amount of balance needs to be maintained in the account to keep it active.

- Checking Account: These are similar to saving accounts, but no interest is earned in this account. These are used for everyday spending. However, unlike a savings account, there is no limit for withdrawal in a checking account.

- Money Market Account: This account gives combined benefits of both saving and checking accounts. They let you earn higher interest rates. These accounts are best suited for people with high bank balances. The high-interest rates make these accounts a better option than checking accounts. However, many banks offer high-interest checking accounts that offer better interest rates than money market accounts but impose more restrictions.

- Certificate of Deposits Account: The CD accounts let you deposit your money for a fixed period of time, and in return, bank provides huge interest rates in it. The interest rates offered in these accounts are higher than any other account. However, money needs to be kept in it for a full term or through the end of the 'maturity date'. Withdrawing money before the maturity date will lead to a withdrawal penalty. Hence, this type of account is best for saving for finances planned for the long term.

Q11. What is a crossed cheque?

Knowledge about cheques is highly recommended for candidates. A crossed cheque is a paper cheque that is crossed with two parallel lines either on the top left-hand corner or across the whole paper cheque. It is done to specify an instruction that the cheque must be deposited directly into the mentioned bank account with a bank. A crossed cheque cannot be immediately cashed over the bank counter by the person who possesses it. On the other hand, an open cheque is one that is not crossed and can be cashed at the bank counter.

Q12. What do you know about Banking Ombudsman Scheme?

Bank-related questions include major schemes and policies related to the banking sector. As far as this scheme is concerned, the banking ombudsman scheme addresses the grievances of customers and their complaints concerning any service provided by the bank.

Banking Ombudsman help in the rapid settlement of customer grievances. It was initially introduced under Section 35 A of RBI's Banking Regulation Act, 1949, and came into effect in 1995. It was later amended and became Banking Ombudsman Scheme, 2006. All banks in India are covered under the scheme.

It is important to note that any developments related to policies and schemes of the banking sector must be prepared well by the candidate and must be shared during the interview when required. This not only helps to update your knowledge but also lays a good impression on the interview panel.

Q13. What is the importance of NABARD in India?

This question is indirectly related to banking services in rural areas. This makes it an important topic for banking interview questions. Here is some information about NABARD. It stands for National Bank for Agriculture and Rural Development. It was founded in 1982 as a statutory body with a primary focus on the rural economy of India. NABARD is majorly involved in the following:

- It aims at building a financially inclusive rural India.

- It gives refinance support for building rural infrastructure.

- It formulates credit plans at the district level and guides and the banking industry towards meeting these targets.

- It supervises Cooperative Banks and Regional Rural Banks (RRBs) and helps them to develop good banking practices.

- NABARD international partnerships play an important role in the uplifting of rural communities through training, investments, technology sharing, etc.

- NABARD provides refinance to Regional Rural Banks for lending.

Q14. What is Core Banking Solution?

This is a basic question that you are expected to know. Core Banking Solution or CBS creates a networked bank branch. It helps customers to operate their bank accounts and avail of banking services from any branch of the bank irrespective of the place the bank account is maintained. Hence, the customer is no more restricted to avail banking services of one specific branch.

Do you know? CORE banking stands for 'Centralised Online Real-time Exchange'

You must not confuse core banking with retail banking. The two banking terms are interrelated but are different from each other. Retail banking is everyday banking that happens between consumers and their personal banks offering consumers basic banking services, such as checking accounts, savings accounts, loans, and more.

Q15. Is Core Banking Solution different from Internet Banking?

For bank interviews, it is important to understand the key difference between important banking-related terms. Core Banking Solutions and Internet Banking are different facilities.

| Core Banking Services | Internet Banking Services |

| Through Core Banking Services, the account information is centralized to the bank server instead of being stored at a single branch. It employs large centralized servers that store account-related information from all the branches of a particular bank. |

Internet Banking Services allow customers to perform monetary transactions online using their portable devices. It is quite often called mobile banking- a service that helps people with online bill payments, interbank deposits, and other types of financial transactions. It requests information access from the main bank server and stores it in the user application for instant use. |

Q16. Name some public sector banks.

Such bank interview questions must be at your fingertips. The idea is not to get confused between the public sector and private sector banks. For your conceptual clarity, in public sector banks major stakes are with the government and in private banks majority of the stakes are with the shareholders of the bank. Both types of banks are involved in granting long-term and short-term loans, deposits, financial assets, etc.

Examples of some public sector banks are the State Bank of India, UCO Bank, Bank of India, Canara Bank, Bank of Baroda, etc. These are some of the largest banks. HDFC, ICICI, and IDFC are some of the private sector banks.

Q17. What Is Brown Label ATM and White Label ATM?

This bank interview question can be a tricky one in case you don't know anything about it. Hence, it is always recommended that you read the uncommon facts and information in order to keep yourself updated. Actually, Brown Label ATM is where investment, installation, and maintenance are done by a private operator but the license and branding are with a commercial bank. On the other hand, White Label ATM is owned by private operators who are seeking to earn commission from the banks for transactions made by their customers.

Q18. Define Marginal Standing Facility.

Marginal Standing Facility is a window for banks to borrow from the Reserve Bank of India in an emergency from RBI for up to 24 hours when the inter-bank liquidity dries up completely. This scheme is launched by RBI and is always 1% above the repo rate.

Q19. List a few financial assets.

A financial asset is a non-physical asset whose value is derived from contractual agreements. Following are some of the financial assets:

- Cash (and its equivalents)

- Fixed deposits

- Bonds and debentures

- Equity shares

- Mutual funds

Q20. Explain Statutory Liquidity Ratio and Cash Reserve Ratio.

Such questions are one of the basic bank interview questions. By definition, the Statutory Liquidity Ratio is the amount of Net Demand and Time Liabilities (NDTL) that a bank needs to maintain in the form of cash, gold, or government securities before giving loans to its customers. It is a way through which RBI ensures that bank maintains a reserve amount out of their deposits to meet any future contingencies. Cash Reserve Ratio is the reserve cash of the bank deposited with the RBI. CRR helps RBI in regulating liquidity in the market.

Q21. What do you mean by Para Banking?

Para Banking includes all the ancillary services provided by banks apart from day-to-day banking. These are insurance products, debit cards, credit cards service, cash and credit management services, etc.

Q22. Differentiate between check and demand draft?

Cheque is a negotiable instrument that is paid to the bearer. On the other hand, a demand draft is a pre-paid non-negotiable instrument that the drawee bank undertakes to make payment in full when the same is presented by the payee for payment at the bank.

Q23. What are prime rates?

Prime rate, also called prime lending rate, is the interest rate that large commercial banks charge from their preferred customers with a high credit score or highest credit rating as per the loan grading system. Often these customers are large corporate organizations.

Q24. Discuss banking reforms in the Indian Banking sector.

This bank interview question needs an overall balanced view of the Indian banking sector. You can say that the Indian banking sector has been constantly evolving. It has been focusing a lot on social reform and financial inclusion. However, issues such as large repayment risk, the decline in asset quality, and bad loans have affected the industry badly. These issues need to be kept in check to strengthen the banking system. There is a need for the banking sector to improve its resilience and maintain financial stability.

Keeping this in view, the government has announced new banking reforms, under which the establishment of a Development Finance Institution and Bad Bank has been proposed. Privatization of public banks has been done to facilitate the mobilization of additional capital. Steps such as these will be quite helpful for the Indian banking sector.

Q25. What are the functions of RBI?

RBI was established as a financial institution in 1935 and works as the central bank of India. Its main functions include:

- Issuance of currency notes

- Acting as banker's bank and banker to the government

- Maintains foreign exchange reserves

- Maintains liquidity in the market through CRR and SLR

- It is the controller of credit and lender of last resort

- It helps secure monetary stability in India and maintains India's credit system for a sound financial situation.

Q26. What is an equity loan?

Equity is the monetary value of a property. Hence, an equity loan is a loan that is available to a person against the equity on a property. The loan amount is determined by the value of the property and so it is also called a home equity loan. In short, the equity of the home is used as collateral to get a loan.

Q27. Define cost of debt?

Cost of debt is the effective interest rate that a company pays on its long-term debt obligations. It gives investors an idea of a company’s risk level as compared to other companies because companies that are facing high risk generally have a higher debt cost.

Q28. Explain what are Non-Performing Assets (NPA) of a company.

Since NPA' are often in news, there is a high probability that you may face one to two bank interview questions related to NPA during your job interview. Coming to this question, a non-performing asset (NPA) is a loan for which the principal or interest payment has remained overdue for a period of 90 days. It is thus a financial obligation payable to the bank which has not been made or the interest and the principal amount have not been paid in the due period of time. It can also be said as the credit provided by the bank to its customers that could not be recovered in due time. Non-Performing Assets can also be called 'Bad Debt.'

Q 29. What is a balloon payment?

This is one of the interesting and trickiest bank-related questions. As per definition, a balloon payment is a larger-than-usual one-time payment at the end of the loan term. Usually, a balloon payment is more than twice the loan’s average monthly payment. Most of balloon loans require one large payment that pays off the remaining balance at the end of the loan term.

Q 30. What is bank rate?

Another question from the list of frequently asked bank interview questions. Bank rate is the rate charged by the central bank for lending funds to commercial banks. Please note that the bank rate is different from the repo rate as bank rate is charged against loans offered by the central bank to commercial banks but the repo rate is charged for repurchasing the securities sold by the commercial banks to the central bank. Also, bank rate while charging bank rate no collaterals are involved while the repo rate involves securities, bonds, and agreements as collateral.

Piece of advice for facing bank interview questions

During your banking interview, the hiring manager aims to assess your skills and professional experience in banking if any. Hence, you need to be prepared for anything. So no matter what your academic qualifications are, confident body language, good eye contact, and a tight grip on your basic concepts and banking terms are keys to your success in the interview.

Also, to nail all the bank interview questions, keep your knowledge updated about the financial situation of the country and banking policies through newspapers and informative magazines. You may attend mock interviews or read questions with sample answers before your final round. This will help you to deal with high-pressure situations with ease and come up with the correct answer within no time.

You may also like to read:

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Blogs you need to hog!

How To Write Finance Cover Letter For Morgan Stanley (+Free Sample!)

Unstop

55+ Data Structure Interview Questions For 2026 (Detailed Answers)

Muskaan Mishra

How To Negotiate Salary With HR: Tips And Insider Advice

Srishti Magan

80+ TCS NQT Interview Questions & Answers (2026) You Must Prepare

Urvashi Singhal

Comments

Add comment