Asian Paints Alchemy 2026

Table of content:

- CRR Vs SLR: Definition & Significance

- CRR Vs SLR: Key Differences & Similarities

- Role Of CRR In Monetary Policy

- Role Of SLR In Maintaining Liquidity

- CRR Vs SLR: Advantages & Disadvantages

- CRR & SLR In India

- Frequently Asked Questions (FAQs)

Difference Between CRR And SLR: Definition & Role Explained

Understanding CRR & SLR is essential in the areas of banking and finance. These tools of the economy are employed to reduce a bank’s lending capacity and manage the money flow in the market.

In the realm of banking and finance, understanding the difference between the Cash Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR) is vital. Both these ratios are regulatory measures employed by central banks, such as the Reserve Bank of India (RBI), to control the money supply and regulate credit flow in an economy. By mandating these ratios, financial stability can be maintained while ensuring banks have sufficient capacity to meet depositor demands. This article delves into the definitions, key differences, and roles associated with CRR and SLR, shedding light on their significance within the broader framework of monetary policy.

CRR Vs SLR: Definition & Significance

The Cash Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR) are two important tools used by central banks to regulate the liquidity in the banking system. They formed primary tools in the economy, which reduces the bank’s lending capacity and manages the money flow in the market. While both tools serve a similar purpose, they have distinct differences in their meaning and significance.

Cash Reserve Ratio

The Cash Reserve Ratio (CRR) is a percentage of the total deposits that banks are required to keep as cash reserves with the central bank. This ratio ensures that banks have adequate cash reserves to meet depositor withdrawals. Essentially, CRR represents the minimum percentage of deposits that a commercial bank must keep as a cash reserve with the RBI. The CRR aims to control the credit-creating capacity of the banks by instructing them to keep a certain proportion of the deposits as reserves with the RBI.

Image credit: Freepik

The primary objective of CRR is to maintain financial stability by preventing excessive lending and ensuring that banks have enough liquid assets on hand. CRR helps control inflation by reducing the amount of money available for lending, thereby curbing excess liquidity in the economy. It acts as a monetary policy tool for regulating credit growth. When the central bank increases the CRR, it reduces the amount of funds available for commercial banks to lend, which can lead to higher interest rates and slower economic growth.

Statutory Liquidity Ratio (SLR)

The Statutory Liquidity Ratio (SLR) is another requirement set by central banks that mandates commercial banks to maintain a certain percentage of their net demand and time liabilities in specified liquid assets such as government securities. In other words, SLR is a percentage of net time and demand liabilities kept by the bank in the form of liquid assets. Time Liabilities mean the amount of money that is made payable to the customer after a period of time while demand liabilities mean the amount of money that is made payable to the customer at the time when it is demanded. This ensures that banks have sufficient liquid assets on hand to honor their obligations. SLR helps maintain stability in the financial system by ensuring that banks have enough liquid assets to meet their short-term obligations. It acts as a safeguard against liquidity risks. When the central bank increases the SLR, it reduces the amount of funds available for lending, similar to CRR. This can impact interest rates and credit availability in the economy.

Both CRR and SLR play indispensable roles in maintaining liquidity, controlling inflation, and managing monetary policy. They act as safeguards against excessive lending by banks, promoting stability in the financial system.

CRR Vs SLR: Key Differences & Similarities

CRR and SLR are both reserve requirements imposed on banks, but they serve different purposes.

Difference Between CRR And SLR

Let's delve into the key difference between between CRR and SLR

|

CRR |

SLR |

|---|---|

|

CRR is the percentage of net demand and time liabilities (NDTL) that banks are required to keep with the central bank in the form of cash reserves. |

SLR is the percentage of net demand and time liabilities (NDTL) that banks are required to maintain in the form of liquid assets like cash, gold, or government securities. |

|

CRR is used to control the liquidity in the economy and to ensure that banks have enough funds to meet their obligations. |

SLR is used to ensure the solvency of banks and to regulate credit flow in the economy. |

|

CRR directly impacts the liquidity of banks as it requires them to keep a certain percentage of their deposits as cash reserves. |

SLR indirectly impacts the liquidity of banks as it requires them to maintain a certain percentage of their deposits in the form of liquid assets. |

|

Banks do not earn any interest on the cash reserves held under CRR. |

Banks can earn interest on the liquid assets held under SLR, such as government securities. |

Similarities

Now that we’ve studied the difference between CRR and SLR, let’s take a look at the similarities between the two:

|

CRR |

SLR |

|

Regulated by the Reserve Bank of India (RBI) |

Regulated by the Reserve Bank of India (RBI). |

|

Banks are penalized if they fail to maintain the required CRR. The penalty is charged at a rate higher than the prevailing interest rate. |

Banks are penalized if they fail to maintain the required SLR. The penalty is charged at a rate higher than the prevailing interest rate. |

|

The CRR rate is set by the central bank and can be changed at any time. |

The SLR rate is also set by the central bank and can be changed at any time. |

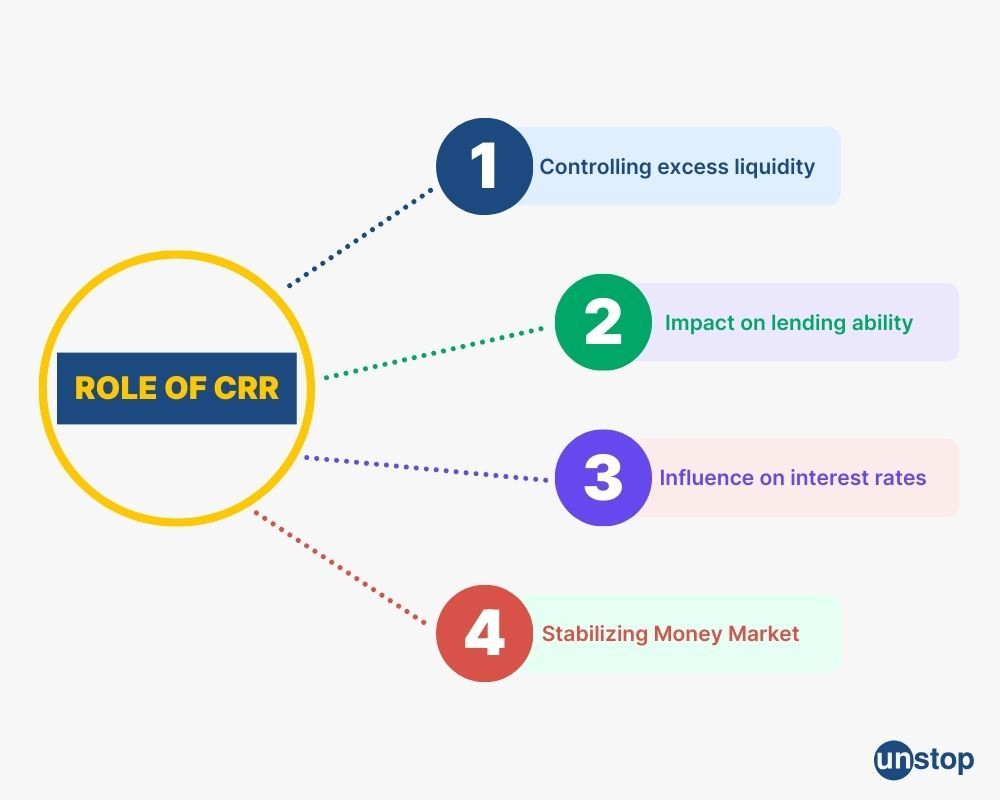

Role Of CRR In Monetary Policy

The Cash Reserve Ratio (CRR) plays an essential role in the monetary policy of a country. Its primary objective is to control inflation by managing the liquidity in the banking system. Let's explore how it accomplishes this and its impact on the overall economy.

Controlling Excess Liquidity

One of the main purposes of CRR is to regulate excess liquidity in the banking system. When banks have surplus funds, they tend to lend more, which can lead to an increase in money supply and inflationary pressures. By mandating that commercial banks maintain a certain percentage of their deposits as reserves with the central bank, CRR helps curb excessive lending and keeps inflation under control.

Impact On Lending Ability

Adjustments made to the CRR directly affect a bank's ability to lend money. When the central bank increases the CRR, it reduces the available funds for lending purposes. As a result, commercial banks have less money to lend out, which can slow down credit growth in the economy. Conversely, when the central bank decreases the CRR, it frees up more funds for lending, stimulating credit expansion.

Influence On Interest Rates

Changes in CRR also have an impact on interest rates charged on loans and deposits. When banks are required to keep a higher proportion of their deposits as reserves, they have less money available for lending. This scarcity of funds drives up borrowing costs and leads to higher interest rates on loans for consumers and businesses alike.

Conversely, lowering the CRR increases banks' lending capacity and injects more liquidity into the market. This increased availability of funds can lower interest rates on loans, making borrowing more affordable for individuals and businesses.

Managing Liquidity & Stabilizing Money Market

The central bank uses CRR as a tool to manage liquidity in the banking system effectively. By adjusting this ratio periodically based on economic conditions and objectives, the central bank can ensure that there is an optimal level of liquidity in the money market. This helps stabilize interest rates and maintain overall financial stability.

CRR also acts as a safeguard against potential banking crises. By mandating banks to keep a certain percentage of their deposits as reserves, it ensures that they have sufficient funds to meet any unforeseen liquidity demands or financial shocks.

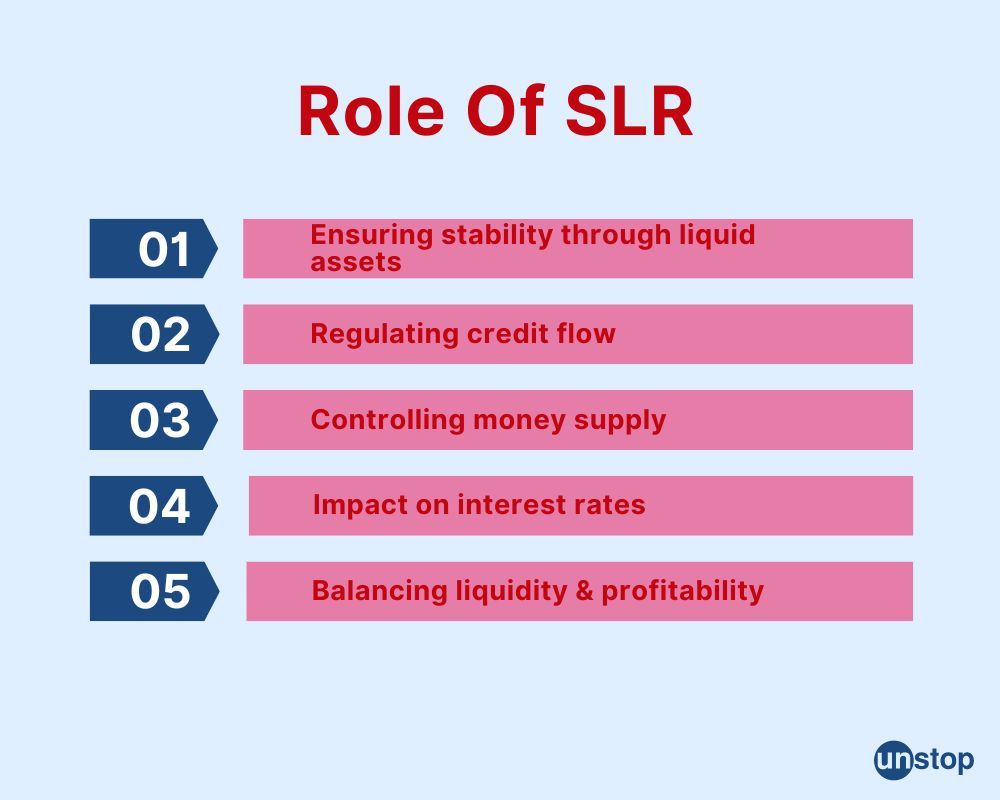

Role Of SLR In Maintaining Liquidity

The Statutory Liquidity Ratio (SLR) plays a crucial role in ensuring the stability and liquidity of banks. It requires banks to maintain a certain percentage of their net demand and time liabilities in liquid assets. Let's delve into the significance of SLR and how it helps maintain liquidity in the financial system.

Ensuring Stability Through Liquid Assets

One of the primary purposes of SLR is to ensure that banks have enough liquid assets on hand to meet depositor demands promptly. By investing in government securities or approved securities, banks contribute to the stability of the financial system. These liquid assets act as a cushion against liquidity risks, providing solvency to banks even during turbulent times.

Regulating Credit Flow

In addition to maintaining stability, SLR also plays an important role in regulating credit flow within the economy. By controlling excessive lending, SLR helps influence interest rates and ensures that credit is extended responsibly. When banks are required to maintain a higher SLR, it reduces their lending capacity as they need to hold more liquid assets. This decrease in lending capacity can help prevent an overheating economy and control inflationary pressures.

Controlling Money Supply

SLR indirectly affects the money supply within an economy. When banks increase their holdings of liquid assets to meet SLR requirements, it reduces their ability to lend out money freely. As a result, there is less money flowing into the economy, which can help control inflationary pressures. On the other hand, when SLR requirements are lowered, it frees up more funds for lending, stimulating economic growth.

Impact On Interest Rates

Changes in SLR can also have an impact on interest rates within the banking system. When SLR requirements are increased by regulatory authorities, banks have fewer funds available for lending purposes. This reduction in available funds may lead to higher interest rates as borrowers compete for limited credit resources. Conversely, when SLR requirements are decreased, banks have more funds to lend, which can lead to lower interest rates.

Balancing Liquidity & Profitability

While SLR ensures liquidity and stability in the banking system, it also poses a challenge for banks in terms of profitability. Banks must strike a balance between holding enough liquid assets to meet SLR requirements and maximizing their profits through lending activities. Striking this balance is vital as excessive holdings of liquid assets may limit a bank's ability to generate income from loans.

CRR Vs SLR: Advantages & Disadvantages

Like the difference between CRR and SLR, understanding their advantages and disadvantages is important in comprehending their impact on the economy.

|

Advantages of CRR |

Disadvantages of CRR |

Advantages of SLR |

Disadvantages of SLR |

|---|---|---|---|

|

Helps in controlling inflation |

Reduces profitability of banks |

Provides liquidity to banks |

Limited flexibility for banks |

|

Ensures stability in the banking system |

Increases compliance costs for banks |

Acts as a safety net for banks |

Low returns on investment |

|

Helps in maintaining monetary policy |

Can lead to a shortage of funds for banks |

Promotes long-term investment |

Restricts banks from lending freely |

|

Enables the central bank to manage liquidity |

Can lead to a decrease in credit availability |

Enhances financial stability |

Limits the ability of banks to expand their business |

|

Acts as a tool for monetary policy transmission |

Can create a liquidity crunch in the economy |

Supports the development of government securities market |

Can result in a crowding-out effect on private investment |

CRR & SLR In India

In India, the Reserve Bank of India (RBI) holds the power to determine both the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). These ratios are reviewed periodically by the RBI based on various factors such as economic conditions, monetary policy objectives, inflation levels, and credit growth targets.

Authority Of RBI

RBI is responsible for ensuring that banks operating in India comply with its regulations while maintaining adequate reserves as per prescribed guidelines. The primary objective behind setting these ratios is to regulate liquidity in the banking system and influence credit creation.

Official Notifications

Any changes in CRR or SLR are communicated through official notifications issued by the RBI. These notifications provide banks with clear instructions on revised percentages or any other modifications related to these reserve requirements. Banks are required to adhere to these changes within a specified timeframe.

Compliance By Banks

Banks must ensure compliance with CRR and SLR rules at all times. They need to maintain a certain percentage of their net demand and time liabilities (NDTL) as cash reserves (CRR) and invest a certain percentage of NDTL in approved securities (SLR). Non-compliance can lead to penalties imposed by the RBI.

Conclusion

In conclusion, the difference between CRR and SLR lies in their purpose and implementation. CRR is a tool used by central banks to regulate liquidity in the economy, requiring commercial banks to maintain a certain percentage of their net demand and time liabilities as cash reserves with the central bank. On the other hand, SLR mandates banks to invest a specific portion of their net demand and time liabilities in government securities. By comprehending the variations between CRR and SLR, individuals can gain insights into how these regulations impact monetary policy and maintain liquidity within the banking system. It is essential for both investors and financial institutions to be aware of these differences as they navigate the complex world of finance.

Frequently Asked Questions (FAQs)

1. How does CRR affect interest rates?

CRR indirectly affects interest rates as it reduces the lendable resources of commercial banks. When CRR increases, banks have less money available for lending, which can lead to higher interest rates on loans.

2. Can SLR be used as collateral for borrowing funds?

Yes, SLR investments in government securities can be used as collateral for borrowing funds from other financial institutions or even from the central bank itself.

3. Are there any penalties for non-compliance with CRR or SLR requirements?

Yes, there are penalties imposed on banks that fail to meet CRR or SLR requirements. These penalties can include fines or restrictions on certain banking activities until compliance is achieved as per the official guidelines of the central bank.

4. How often are CRR and SLR ratios revised?

The Reserve Bank of India regularly reviews and revises both CRR and SLR ratios based on prevailing economic conditions. Changes in these ratios aim to manage inflation levels, stimulate economic growth, or address liquidity concerns.

5. What happens if a bank's SLR falls below the mandated level?

If a bank's SLR falls below the mandated level, it must take immediate corrective measures to restore compliance. Failure to do so can result in penalties and regulatory action by the central bank.

Suggested reads:

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment