Asian Paints Alchemy 2026

Table of content:

- What Is The Law Of Supply In Economics?

- Types Of Law Of Supply In Economics

- Importance Of The Law Of Supply

- What Is The Formula For The Law Of Supply?

- Relationship Between Price & Supply

- Factors Influencing The Law Of Supply

- Impact Of Different Goods On Supply & Demand

- Examples Of The Law Of Supply In Action

- Conclusion

- Frequently Asked Questions (FAQs)

Law Of Supply | Definition, Types, Formula And Examples Explained

The Law of Supply helps us understand how businesses respond to changes in market conditions by recognizing the relationship between price and quantity supplied. Read on for more.

The law of supply is essential for figuring out how much of a product will be available and at what price in a market. It influences how sellers and producers act. When prices go up, businesses are encouraged to make more products because they can earn greater profits. On the other hand, if prices drop, producers might cut back on production or even leave the market entirely.

In this article, we will delve into the details of the law of supply, covering its meaning, formula, different types, and various influencing factors.

What Is The Law Of Supply In Economics?

The Law of Supply is a fundamental economic principle that describes how the quantity of a good or service that producers are willing to produce changes in response to variations in price. Specifically, the law posits that all else being equal, an increase in the price of a good leads to an increase in the quantity supplied, while a decrease in price results in a decrease in the quantity supplied.

This positive relationship exists because higher prices typically incentivize producers to increase production as the potential for greater revenue becomes more appealing. Conversely, lower prices can make production less attractive, leading to a reduction in supply.

It helps us understand how businesses respond to changes in market conditions by recognizing the relationship between price and quantity supplied. Accordingly, producers can adjust their production levels to meet market demand.

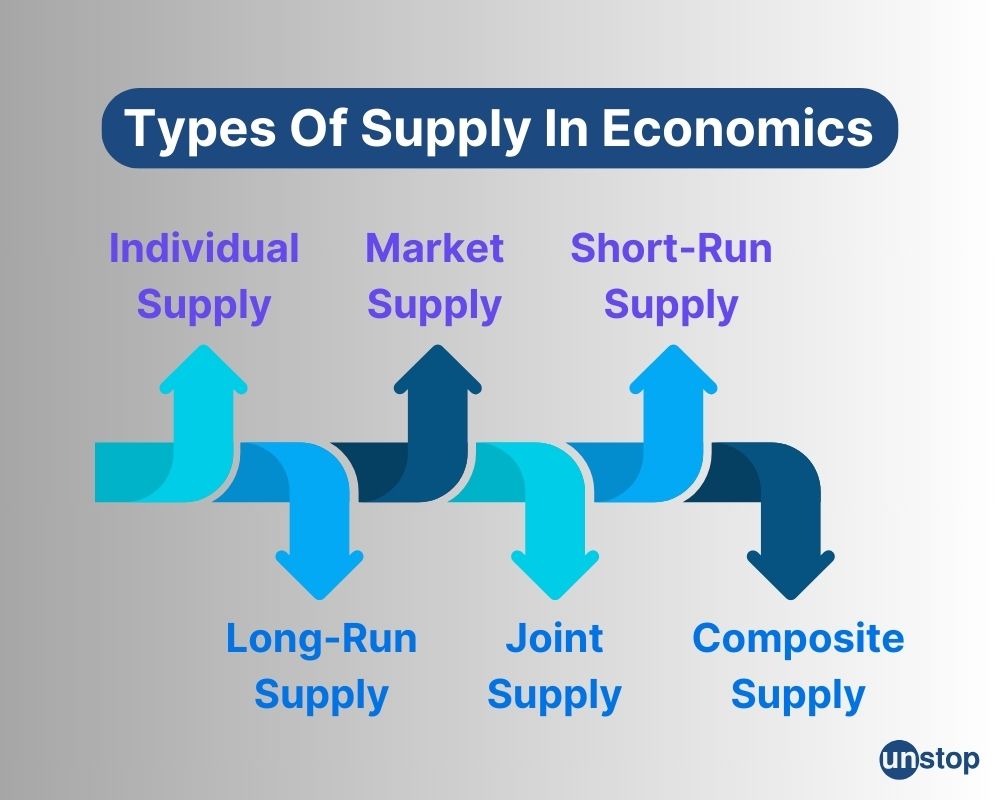

Types Of Supply In Economics

Although the main idea of the Law of Supply is the same, various situations can change our understanding of supply. Here are some related viewpoints or types of the Law of Supply:

Individual Supply

The individual supply states the quantity of a good that a single producer or firm is willing to supply at different prices. This supply curve illustrates the relationship between the price and quantity supplied by one specific entity.

It helps in understanding the production decisions of individual firms, considering their specific costs, resources, and constraints.

Market Supply

Market supply is the total quantity of a good that all producers in a market are willing to supply at various price levels.

It is derived by horizontally summing the individual supply curves of all producers. This aggregate view is crucial for understanding overall market behaviour and for determining market equilibrium.

Short-Run Supply

The short-run supply refers to the supply of goods in a period during which at least one factor of production is fixed. In the short run, firms cannot adjust all inputs, such as capital or plant size.

The supply curve in this context shows how much firms are willing to supply given these constraints. Typically, the short-run supply curve is more inelastic because firms have limited flexibility to change production levels.

Long-Run Supply

Long-run supply refers to the supply of goods when all production factors are variable, and firms can fully adjust their production processes. Firms can enter or exit the market, expand or reduce their production capacity, and adopt new technologies in this type of supply.

The long-run supply curve is usually more elastic than the short-run supply curve because firms have greater flexibility to respond to changes in price.

Joint Supply

The joint supply is one where the production of one good simultaneously leads to the production of another good. This is common in industries where the production process yields multiple products, such as in the production of beef and leather.

The supply relationship here is interconnected, making it important to consider the joint nature of the production process as any changes in the price of one product can affect the supply of the other.

Composite Supply

Composite supply refers to a scenario where a particular good can be supplied from different sources or through different processes. For example, electricity can be generated from coal, hydro, nuclear, or renewable sources.

The overall supply of electricity is a composite of these various sources. Changes in the costs or availability of any one source can impact the composite supply.

Importance Of The Law Of Supply

The Law of Supply provides foundational insights into market behaviour and guiding decision-making for producers, consumers, and policymakers. Here are the top five importance of this law:

1. Understanding Market Dynamics

The Law of Supply helps in understanding how market dynamics work, particularly the behaviour of producers in response to price changes. It explains why producers are willing to supply more of a good when its price rises and less when its price falls, offering a foundational explanation for market supply curves and price-setting mechanisms.

2. Guiding Production Decisions

For businesses, the Law of Supply is crucial for making production decisions. Firms can better anticipate how changes in market prices might affect their production levels and revenues. This understanding allows businesses to optimize production schedules, manage inventory, and allocate resources efficiently.

3. Basis for Pricing Strategies

The Law of Supply provides a basis for developing pricing strategies. Knowing that an increase in price typically leads to an increase in quantity supplied, firms can use this relationship to adjust prices in a way that balances demand and supply, maximizes revenue, and avoids surpluses or shortages. It assists in determining prices that take into account production costs and the profits a business aims to achieve.

4. Policy Formulation & Economic Planning

Policymakers use the Law of Supply to understand and predict the effects of various economic policies, such as taxes, subsidies, and regulations, on the supply of goods and services. By anticipating how producers will respond to these policies, governments can craft measures that promote economic stability, encourage production, and manage inflation.

5. Foundation for Economic Models & Theories

The Law of Supply is a fundamental component of many economic models and theories, including supply and demand analysis, equilibrium pricing, and market competition. This law is a basic idea that helps explain more complicated economic theories about how markets work, how resources are used, and how economies grow. Knowing this law is important for anyone learning about economics because it supports many key concepts in the field.

What Is The Formula For The Law Of Supply?

The formula for the Law of Supply is often shown using a supply function. This function illustrates how much of a product or service producers are ready to offer based on its price.

The general formula for the supply function is Qs=f(P)

Here,

Qs is the quantity supplied.

P is the price of the good.

f denotes the functional relationship between price and quantity supplied.

In a more specific linear form, the supply function can be written as Qs=c+dP

Here,

Qs is the quantity supplied.

P is the price of the good.

c is the intercept on the quantity axis, representing the quantity supplied when the price is zero. It can be zero or negative, depending on the context.

d represents the slope of the supply curve, representing the rate at which the quantity supplied changes with a change in price.

In the context of the Law of Supply, d is typically positive, indicating that as the price increases, the quantity supplied also increases.

Relationship Between Price & Supply

When the price of a product increases, suppliers are motivated to increase their production in order to take advantage of higher profit opportunities. Conversely, when prices fall, suppliers may reduce their output as it becomes less profitable for them.

One reason for this positive relationship between price and quantity supplied is the concept of profit maximization. Suppliers aim to maximize their profits by producing goods or services that yield the highest returns.

When prices rise, profit margins increase, providing an incentive for suppliers to expand their production capacity and meet the growing demand.

Suppliers consider factors such as production costs and resource availability when determining their output levels. Higher prices can offset increased costs associated with raw materials, labour, or other inputs required for production. This allows suppliers to maintain profitability while meeting market demand.

Factors Influencing The Law Of Supply

Several factors can influence this relationship between price and supply. Let's explore some of the important factors that influence the law of supply.

Input Costs

One key factor that influences the law of supply is input costs. These refer to the expenses incurred by producers in order to create their goods or services. Input costs include things like raw materials, labor wages, energy costs, and transportation expenses. When input costs rise, it becomes more expensive for suppliers to produce their goods or services.

If the cost of raw materials used in manufacturing a product increases significantly, it will result in higher production costs for suppliers. As a result, they may reduce the quantity supplied unless they can pass on these increased costs to consumers through higher prices.

Technology Usage

Using the latest technological advancements contributes to shaping the law of supply. Innovation and improvements in technology can lead to increased productivity or reduced production costs for suppliers. This can have a positive impact on supply.

A company implementing automated machinery in its manufacturing process can increase its production capacity without requiring additional labour.

Regulations

Changes in government regulations can also affect suppliers' ability or willingness to produce goods. Regulations related to environmental standards, safety requirements, or quality control measures can impose additional costs on producers and potentially limit their ability to supply goods.

Suppose new regulations are introduced that require manufacturers to implement costly pollution control measures. In such cases, producers may face increased compliance costs and decide to reduce their output due to financial constraints.

Taxes

In addition to regulations, changes in taxes imposed on businesses can impact supply as well. Higher taxes can reduce a supplier's profit margin, making it less attractive to produce and supply goods.

If the government increases taxes on a specific industry, such as the tobacco industry, suppliers may face higher costs. This could lead to a decrease in the quantity supplied as producers try to maintain their profit margins.

Expectations of Future Prices

Producers' expectations about future prices can affect how much they supply now. If they think prices will go up later, they might provide less now to sell more at higher prices in the future.

If producers expect prices to fall, they may increase the current supply to sell as much as possible at current higher prices, increasing the present supply.

Natural Conditions

Natural factors, such as weather conditions and natural disasters, particularly affect the supply of agricultural products and other goods dependent on natural resources.

Good weather or abundant natural resources can increase supply (rightward shift of the supply curve). Bad weather, droughts, or natural disasters can reduce supply (leftward shift of the supply curve).

Prices of Related Goods

The supply of a good can be influenced by the prices of related goods, particularly those that are substitutes or complements in production. If the price of a substitute good rises, producers might shift production to that good, reducing the supply of the original good.

If two goods are produced together (joint products), an increase in the price of one can increase the supply of the other.

Impact Of Different Goods On Supply & Demand

Different types of goods have varying impacts on the law of supply. The type of good can affect how quickly producers can respond to changes in demand and adjust their supply accordingly.

Producers of perishable items like fresh fruits, vegetables, and flowers must adapt swiftly to shifts in consumer demand. Since these goods have a limited shelf life and can spoil if not sold promptly, producers must ensure a steady supply to meet consumer needs.

This means that the law of supply is more sensitive to perishable goods compared to durable goods.

For example, imagine there is suddenly a high demand for strawberries due to a popular new recipe going viral on social media. Farmers who grow strawberries need to increase their production rapidly to meet this surge in demand. They may need to hire more workers, acquire additional land for cultivation, or invest in advanced farming techniques to boost their strawberry output quickly.

In contrast, durable goods like furniture or electronics have longer lifespans and are not subject to rapid spoilage. As a result, producers have more flexibility in adjusting their supply based on market conditions. They can take their time and plan production schedules accordingly without the urgency faced by producers of perishable goods.

Examples Of The Law Of Supply In Action

Examples show how the law of supply usually works, but there can be exceptions based on different situations:

Oil Price

When the price of oil goes up, countries that produce oil often ramp up their production to take advantage of the higher profits. This is a prime example of the law of supply in action. These countries understand that when prices rise, it becomes more lucrative to extract and sell oil.

Seasonal Sale

Retailers often prepare for seasonal sales by boosting their inventory. They expect more customers to want to buy products during these times, so having extra stock helps them meet this demand. By increasing their supply, they can also take advantage of higher prices when shoppers are eager to purchase. This approach reflects the law of supply, as businesses modify their inventory based on predictions of changing customer demand.

Electric vehicles

As more people show interest in electric vehicles (EVs), car manufacturers are ramping up their production. They see that the demand for EVs is increasing and want to boost their supply to meet this need. By doing this, these companies can satisfy what customers want while also benefiting from the growth in the market.

Conclusion

In conclusion, the law of supply is a key concept in economics that explains how producers react to changes in price. When the price of a good or service goes up, suppliers tend to offer more of it, and when the price drops, they usually supply less. This principle helps us see how suppliers behave and how price affects the amount available in the market. Supply curves are drawn upwards, showing that higher prices encourage producers to provide more products.

By understanding the law of supply, we can better analyze and predict how changes in price and other factors will impact the quantity of goods or services supplied in a market.

Frequently Asked Questions (FAQs)

1. How does technological advancement affect the law of supply?

Technological advancements can significantly impact the law of supply by increasing productivity levels and reducing production costs. This often leads to an increase in overall supply as businesses can produce more goods or services at a lower cost.

2. Can changes in government regulations influence the law of supply?

Yes, changes in government regulations can have a direct impact on the law of supply. For example, stricter environmental regulations may increase production costs for certain industries, potentially leading to a decrease in supply.

3. What role does the availability of resources play in the law of supply?

.If key resources required for production become scarce or more expensive, it can limit the ability of suppliers to meet demand, resulting in a decrease in supply.

4. How do changes in consumer preferences affect the law of supply?

Changes in consumer preferences can influence the law of supply by altering demand patterns for specific goods or services. Suppliers may need to adjust their production levels accordingly to meet evolving consumer demands.

Suggested reads:

-

Financial Leverage: Definition, Types, Formula, Risks And Benefits

-

Financial Management: Definition, Types, Importance And Functions

-

Dividend: Definition, Types, Examples And Impact On Investments

-

Time Value Of Money: Definition, Formulas, Importance And Methods

-

Cost Of Capital: Definition, Components, Factors, Formula And Role

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment