Asian Paints Alchemy 2026

Aptitude

- Step 1: The Groundwork

- Step 2: The Three Sections

- Step 3: Practice Makes Improvement

- The Secret Ingredient

- Understanding Basics Of Number Series

- Types Of Number Series Reasoning Questions

- Addition & Multiplication In Number Series

- Square & Cube-Based Number Series Patterns

- Missing Terms & Arranging Sequences

- Tricks & Tips For Solving Number Series

- Selected Number Series Questions With Solutions

- Frequently Asked Questions (FAQs)

- Must Know Terminologies in Blood Relation Questions

- Basic Approaches to Solve Blood Relation Questions

- Types Of Blood Relation Questions

- Tips For Solving Blood Relation Questions

- Multiple Choice Questions (MCQs) with Detailed Explanation

- Conclusion

- Frequently Asked Questions (FAQs)

- Letter Series In Logical Reasoning

- Types Of Letter Series Patterns

- Tips For Solving Letter Series Reasoning

- Best Practice Question Samples With Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Basics of Problems On Age-Related Questions

- Formula to Solve Problems on Ages-Related Questions

- Types of Age-Related Questions & Examples

- Tips & Tricks for Solving Ages Problems

- Best MCQs on Problems on ages with solved answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Definition of Calendar

- Understanding Days of the Week

- What is a Leap Year?

- Concept of Odd Days in a Century

- Tips For Solving Calendar Reasoning Questions

- Best Calendar Reasoning Questions with Answers (MCQs)

- Frequently Asked Questions (FAQs)

- Basic Concepts of Clock

- Structure of a Clock

- Angle Equilavalence in Clock

- Tips For Solving Clock Questions

- Selected Clock Questions & Answers (MCQs)

- Conclusion

- Frequently Asked Questions (FAQs)

- Understanding The Concept Of Direction Sense

- Tips For Effective Problem-Solving In Direction Sense

- Practical Test Practice Questions And Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Importance Of Dice Reasoning

- Dice Numbers In Dice Reasoning

- Classification Of Dice

- Constructed Vs Deconstructed Dice

- Tricks & Tips For Solving Dice Problems

- Practice MCQs With Detailed Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Alphanumeric Series Defined

- Alphanumeric Series In Reasoning Tests

- Tips & Strategies For Solving Alphanumeric Series

- Practice Sample Questions With Detailed Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Concept Of Mirror Image Reasoning Explained

- Important Terms In Mirror Image Reasoning

- Types Of Mirror Images

- Identifying Correct Mirror Image

- Finding Clock's Mirror Image

- Tips To Solve Mirror Images

- Selected Practice Questions With Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Concept & Overview Of Input-Output

- Input-Output In Competitive Exams

- Types Of Input-Output Problems

- Strategies, Tips & Tricks For Solving Reasoning Questions

- Selected Practice Questions With Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Importance Of Finding The Odd One Out

- Tricks And Tips

- How to Find The Odd One Out?

- Solved MCQs with Detailed Explanation

- Conclusion

- Frequently Asked Questions (FAQs)

- Understanding Key Concepts

- Exploring Different Ranking Types

- Formula And Application Of Order And Ranking

- Tips For Solving Order & Ranking

- Selected Practice Questions And Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Importance Of Pipes & Cistern Aptitude

- Key Terminologies used in Pipes and Cisterns

- Pipes and Cisterns Formula with Examples

- Pipes and Cisterns Shortcut Tricks

- Tips For Solving Pipes & Cistern Problems

- Selected Questions & Answers For Practice (MCQs)

- Conclusion

- Frequently Asked Questions (FAQs)

- Key Concept in Boats and Streams

- Formulas Of Boats & Streams

- Distance & Time Formula

- Tips For Solving Boats & Streams Questions

- Selected Practice Questions With Answers (MCQs)

- Conclusion

- Frequently Asked Questions (FAQs)

- Concept of Mixture and Alligation

- Types Of Alligation Questions

- Formula for Solving Mixture & Alligation

- Tips For Solving Mixture And Alligation

- Selected Questions With Answers For Practice

- Conclusion

- Frequently Asked Questions (FAQs)

- Concepts and Definitions Related to Time and Work

- Important Time And Work Formulas

- Tricks and Tips to Solve Time & Work Questions

- Time And Work MCQs with Detailed Solution

- Conclusion

- Frequently Asked Questions (FAQs)

- What is Harmonic Progression(HP)?

- Formula to find the nth Term in Harmonic Progression

- Formula to find the Sum of the nth Term in HP

- What is Harmonic Mean?

- Harmonic Progression Solved Best MCQs

- Conclusion

- Frequently Asked Questions (FAQs)

- What is Mensuration in Maths?

- What are 2D figures in Mensuration?

- What are 3D figures in Mensuartion?

- Basic Terminologies In Mensuration

- Basic 2D Formulas in Mensuration

- Basic 3D Formulas in Mensuration

- 2D vs 3D in Mensuration

- Solved Questions With Solutions (MCQs)

- Conclusion

- Frequently Asked Questions (FAQs)

- Relationship Between Time, Speed And Distance

- Conversion Units Time, Speed And Distance

- Average & Relative Speed: Two Trains Moving in the same or opposite direction

- Solved MCQs on Time, Speed And Distance

- Conclusion

- Frequently Asked Questions (FAQs)

- What is Simplification in Maths?

- BODMAS Rule in Simplification Explained

- Simplification & Approximation Relation

- Key Terms in Simplification

- Examples Of Simplification Techniques

- Simplification Questions With Solved Answers (MCQs)

- Conclusion

- Frequently Asked Questions (FAQs)

- Height And Distance Important Terms

- Right Angled Triangle In Trigonometry

- Trigonometric Ratios

- Solved Examples For Better Understanding

- Height And Distance Applications In Trigonometry

- Height And Distance Practice Questions & Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Defining Interest Types

- Simple Interest Vs. Compound Interest

- Selected Solved Questions & Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Basic Concepts Of Profit And Loss

- Determining Selling Price

- Calculating Discounts

- Formulas For Calculating Profit And Loss

- Examples Of Profit And Loss

- Profit & Loss Questions With Detailed Solution

- Conclusion

- Frequently Asked Questions (FAQs)

- Defining Angle Of Elevation

- Key Terms Used In Angle Of Elevation

- Angle of Elevation Formula with Example

- Angle of Elevation vs. Angle of Depression

- Angle of Elevation MCQs with Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Defining HCF And LCM

- Calculation Methods Of HCF And LCM

- HCF By Prime Factorization Method

- LCM By Prime Factorization Method

- Difference Between HCF And LCM

- HCF & LCM Practice Questions With Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- What is fraction and decimal?

- Understanding Decimal Fraction

- Place Value in Decimal Fraction

- Mathematical Operations with Decimal Fraction

- Practice with Solved Examples

- Summary

- Frequently Asked Questions

- All About Decimals

- All About Fractions

- How to Convert a Decimal into Fraction

- Simple vs Recurring Decimals

- Converting Recurring Decimals to Fractions

- Conversion Charts

- Practice Questions (With Solutions)

- Closing Thoughts

- Frequently Asked Questions

- What is Arithmetic Mean?

- Arithmetic Mean Formula- Ungroup Data & Group Data

- Merits of Arithmetic Mean

- Demerits of Arithmetic Mean

- Alternatives to Arithmetic Mean

- What is the Weighted Arithmetic Mean?

- Arithmetic vs. Geometric Mean

- Arithmetic Mean Application in Statistical Analysis

- Arithmetic Mean Practice Questions with Explanation

- Frequently Asked Questions

- What is Geometric Progression?

- Key Properties of Geometric Progression

- General Form Of Geometric Progression

- General Term or the Nth Term of Geometric Progression

- The sum of nth Terms of GP

- Types Of Geometric Progression

- Solved Questions and Answers of GP

- Conclusion

- Frequently Asked Questions (FAQs)

- Average in Maths

- Average Formula in Maths

- Differentiating Types of Average

- How to Calculate Average of Negative Numbers?

- Practical Applications of Averages

- Average Questions For Practice

- Frequently Asked Questions

- What is Simple Interest in Maths?

- Simple Interest Formula Explained

- Simple Interest Formula for Years, Months & Days

- Simple Interest Examples & Practice Questions

- Conclusion

- Frequently Asked Questions (FAQs)

- Defining Mathematical Ratios

- Understanding Proportions Fundamentals

- Differentiating Ratios from Proportions

- Ratio and Proportion Formulas

- Properties of Ratio and Proportion

- How to Solve Ratio and Proportion Problems

- Ratio and Proportion Problems (With Solutions)

- Summary

- Frequently Asked Questions

- What is Number in Maths?

- Types of Numbers With Example

- Real vs Complex Numbers Explored

- Basic Operations on Numbers

- Practice Questions (With Solutions)

- Frequently Asked Questions

- What is Arithmetic Progression (AP) in Maths?

- Important Terminologies in Arithmetic Progression

- Basic Terms in Arithmetic Progression

- General Form Of Arithmetic Progression Series

- Types Of Arithmetic Progression

- Solved Questions With Explanation (MCQs)

- Conclusion

- Frequently Asked Questions (FAQs)

- Understanding Basic Concept

- Importance Of Train Problems In Aptitude

- Tips To Solve Train Problems

- Selected Practice Questions & Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Definition Of Mode

- Calculating Mode For Ungrouped Data

- Calculating Mode For Grouped Data

- Bimodal, Trimodal & Multimodal Distributions

- Comparing Mean, Median & Mode

- Selected Practice Questions With Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Important Concept In Races And Games

- Calculating Time, Speed & Distance

- Importance Of Races And Games Problems

- Sample Practice Questions With Answers

- Conclusion

- Frequently Asked Questions (FAQs)

- Types Of Partnership

- Formula For Partnership Questions

- Tips To Solve Partnership Aptitude Questions

- Selected Partnership Questions (Practice MCQs)

- Conclusion

- Frequently Asked Questions (FAQs)

Difference Between Simple Interest And Compound Interest (Bonus: Solved QnAs)

Discover the key difference between simple interest and compound interest and learn how they impact your financial decisions! Read on for detailed information.

Grasping the difference between simple interest and compound interest is crucial in financial decision-making. Simple interest involves calculating interest solely on the principal amount, while compound interest considers both the principal and accrued interest. By comprehending these concepts, individuals can make informed choices to optimize their financial outcomes.

Defining Interest Types

To begin with, let us understand the definitions of interest types in detail:

Simple Interest

Simple interest is a direct method of calculating interest, commonly used for short-term loans or investments. It is calculated solely on the principal amount without considering any previously earned interest.

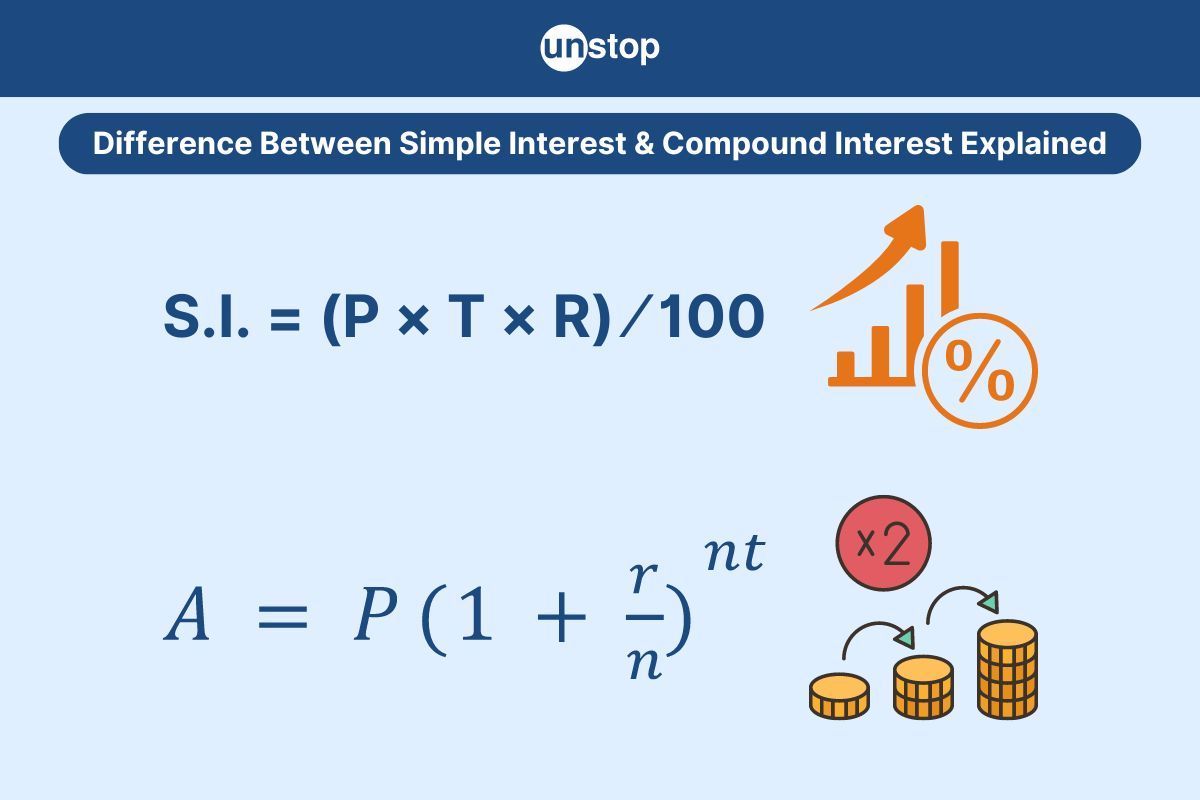

Formula: S.I. = (P × T × R) ⁄ 100

For example, if you borrow ₹1000 at a simple interest rate of 5% per year, you will pay ₹50 in interest annually.

One of the key characteristics of simple interest is its linear growth. This means that the amount of interest earned or paid remains constant over time since it is based only on the original principal amount.

Compound Interest

Compound interest involves calculating interest on both the principal amount and any accumulated interest. This results in a snowball effect where your money grows faster over time compared to simple interest.

Formula: C.I. = P(1+r⁄n)nt

For instance, if you invest ₹1000 at an annual compound interest rate of 5%, your investment will not only earn ₹50 in the first year but also additional earnings on that ₹50 in subsequent years.

When you invest or borrow using compound interest, you earn or pay interest not just on the initial sum but also on any previously earned or charged interest.

Simple Interest Vs. Compound Interest

Let us now see the basic difference between simple interest and compound interest:

Simple Interest |

Compound Interest |

|---|---|

| Formula: (P x r x t)/ 100 | Formula: P x (1 + r/n)nt |

| Interest is calculated only on the principal amount | Interest is figured out based on both the original amount and the interest that has been added. |

| Linear growth | Exponential growth |

| Easier to calculate and understand | Higher returns over time |

| Interest is calculated once per period | Interest is calculated multiple times per period based on compounding frequency. |

Click here to enhance and upskill your quantitative aptitude in simple and compound interest right away!

Selected Solved Questions & Answers

Below are some selected and solved questions and answers related to simple and compound interest. Practice and improve your knowledge in a consistent manner:

Question 1. Calculate the simple interest earned on a principal amount of ₹5000 at an interest rate of 3% per annum for a period of 2 years.

Solution: To solve the question, we can use the formula:

Simple Interest = (Principal amount x Rate x Time) / 100

Simple Interest = (5000 x 3 x 2)/ 100

= 30000 / 100

= 300

Therefore, the simple interest earned on a principal amount of ₹5000 at an interest rate of 3% per annum for a period of 2 years is₹300.

Question 2: If ₹500 is invested at an annual interest rate of 4%, how much interest will be earned after 3 years?

Solution: Principal amount (P) = ₹500

Annual interest rate (R) = 4% = 0.04 Time

(T) = 3 years

Simple Interest (I) = P x R x T

= 500 x 0.04 x 3

=60

Therefore, the interest earned after 3 years will be ₹60.

Question 3: If ₹500 is invested at an annual simple interest rate of 8%, calculate the interest earned after 3 years.

Solution: Principal (P) = ₹500

Rate (R) = 8%

Time (T) = 3 years

Simple Interest (SI) = P x R x T / 100

= 500 x 8 x 3 / 100

= 120

Therefore, the interest earned after 3 years will be₹120.

Question 4: If ₹5000 is invested at an annual interest rate of 6%, how much interest will be earned after 3 years using simple interest?

Solution: Simple Interest = Principal (P) x Rate (R) x Time (T)

For the given question, the simple interest = 5000 x 0.06 x 3= 900

Therefore, the total interest earned after 3 years would be ₹900.

Question 5: John invested ₹5000 in a savings account for 3 years. In the first year, he earned a simple interest of 5%; in the second year, he earned 7%; and in the third year, he earned 10%. How much money did John have in his account at the end of the third year?

Solution: First-year simple interest = 5000 x 5% = ₹250

Amount after first year = 5000 + 250 = ₹5250

Second-year interest = 5250 x 7% = ₹367.50

Amount after second year = 5250 + 367.50 =₹5617.50

Third-year interest = 5617.50 x 10% = ₹561.75

Total amount after third year = 5617.50 + 561.75 = ₹6179.25

Therefore, John had ₹6179.25 in his account at the end of the third year.

Question 6: If you invest ₹5000 in an account that offers a compound interest rate of 5% per year, how much money will you have after 5 years?

Solution: To solve this problem, we can use the formula for compound interest:

A=P×(1+n/r)nt

Now, according to the question:

P = ₹5000

r=5%=5/100=0.05

n=1 (interest compounded annually)

t=5 years

A=5000×(1+0.05/1)(1×5)

=5000×(1.05)5

A=5000×(1.27628)

A≈6381.40

So, after 5 years, you would have approximately ₹6381.40 in the account.

Question 7. If you invest ₹8000 in an account that offers a compound interest rate of 4% per year, compounded semi-annually, how much money will you have after 3 years?

Solution: According to the question,

- P = ₹8000

- r=4%=0.04 (decimal)

- n=2 (interest compounded semi-annually)

- t=3 years

Putting these values into the formula:

A=8000×(1+0.04/2)(2×3)

A=8000×(1.02)6

Now, calculate A:

A=8000×(1.126825)

A≈9014.60

So, after 3 years, you would have approximately ₹9014.60 in the account.

Question 8: If you invest ₹10,000 with an annual interest rate of 6%, compounded quarterly, how much money will you have after 7 years?

Solution: According to the question,

- P = ₹10,000

- r=6%=0.06 (decimal)

- n=4 (interest compounded quarterly)

- t=7 years

Plugging these values into the formula: A=P×(1+r/n)nt

A=10000×(1+0.06/4)(4×7)

A=10000×(1+0.06/4)28

A=10000×(1.015)28

A≈10000×(1.662792)

A≈16627.92

So, after 7 years, you would have approximately ₹16,627.92 in the account.

Question 9: You decide to invest ₹15,000 with an annual interest rate of 8%, compounded monthly. However, after 3 years, you decide to add an additional ₹5,000 to the account. Assuming the same interest rate and compounding frequency, how much money will you have after a total of 6 years?

Solution: Let's first calculate the amount accumulated after 3 years. As per the question,

- Initial investment P1= ₹15,000

- Annual interest rate r = 8% = 0.08

- Compounding frequency n = 12 (monthly compounding)

- Time t1= 3 years

Using the compound interest formula:

A1=P1×(1+r/n)nt1

A1=15000×(1+0.08/12)(12×3)

A1≈15000×(1+0.08/12)36

A1≈15000×(1.0066667)36

A1≈15000×(1.2653166)

A1≈18979.75

After 3 years, the accumulated amount is approximately ₹18,979.75.

Now, let's calculate the amount accumulated after 6 years, considering the additional ₹5,000 investment:

Given:

- Additional investment P2 = ₹5,000

- Time t2 = 6 years (including the initial 3 years)

Using the compound interest formula again:

A2=(A1+P2)×(1+r/n)nt2

A2=(18979.75+5000)×(1+0.08/12)(12×3)

A2≈23979.75×(1+0.08/12)72

A2≈23979.75×(1.0066667)72

A2≈23979.75×(1.718901)

A2≈41205.22

After 6 years, including the additional investment, the accumulated amount would be approximately ₹41,205.22.

Question 10: You invest ₹20,000 in an account with an annual interest rate of 7%, compounded quarterly. After 2 years, you withdraw ₹5,000 from the account. Assuming the same interest rate and compounding frequency, how much money will you have after 5 years from the initial investment?

Solution:

Let's start by calculating the amount accumulated after 2 years:

Given:

- Initial investment P1 = ₹20,000

- Annual interest rate r = 7% = 0.07 (decimal)

- Compounding frequency n = 4 (quarterly compounding)

- Time t1 = 2 years

Using the compound interest formula:

A1=P1×(1+r/n)nt1

A1=20000×(1+0.07/4)(4×2)

A1≈20000×(1+40.07)8

A1≈20000×(1.0175)8

A1≈20000×(1.14156011)

A1≈22831.20

After 2 years, the accumulated amount is approximately ₹22,831.20.

Now, you withdraw ₹5,000 from the account, leaving P2 = 20000 - 5000 = ₹15,000 as the new principal.

Next, let's calculate the amount accumulated after the remaining 3 years:

Given:

- Principal P2 = ₹15,000

- Annual interest rate r = 7% = 0.07 (decimal)

- Compounding frequency n = 4 (quarterly compounding)

- Time t2 = 3 years

Using the compound interest formula:

A2=P2×(1+r/n)nt2

A2=15000×(1+0.07/4)(4×3)

A2≈15000×(1+0.07/4)12

A2≈15000×(1.0175)12

A2≈15000×(1.30773342471)

A2≈19615.00

After 3 additional years, the accumulated amount from the remaining ₹15,000 is approximately ₹19,615.00.

So, after a total of 5 years from the initial investment, you would have approximately ₹19,615.00 in the account.

You can also indulge in a variety of quizzes that enhance the all-round development of your skills and aptitude.

Conclusion

Being aware of the difference between simple interest and compound interest enables one to see how each type impacts financial outcomes. Simple interest offers straightforward calculations, while compound interest has the potential for exponential growth over time.

By grasping these concepts, individuals can make informed decisions regarding finance, investments, loans, or savings. Embracing a detailed understanding of simple and compound interest empowers individuals to optimize their financial strategies for long-term success.

Time For A Short Quiz

Frequently Asked Questions (FAQs)

1. Point out the key difference between simple interest and compound interest.

Simple interest is calculated only on the principal amount, while compound interest includes both the principal and accumulated interest. Compound interest grows faster due to earning interest on previously earned interest.

2. How is simple interest calculated?

To calculate simple interest, you multiply the principal amount by the interest rate and the time period using the formula: Interest = Principal x Rate x Time.

3. Can you explain how compound interest works in practice?

Compound interest involves reinvesting earned interest back into the principal amount. Over time, this leads to exponential growth as each period's earnings contribute to the next period's calculations.

4. What are compounding periods in compound interest?

Compounding periods refer to how often the interest is added to the principal amount. The more frequent compounding occurs within a given timeframe, such as monthly or daily compounding, the higher the effective yield will be.

5. When should one choose between simple and compound interest?

Choose simple interest for short-term loans or when you prefer straightforward calculations. Opt for compound interest for long-term investments or savings goals where maximizing growth over time is crucial. Consider factors like time horizon and financial objectives when deciding between them.

Suggested reads:

- What Is Mensuration: Formulas With Top Selected Question & Answer

- Harmonic Progression- Formula With Selected Questions & Answers

- Mixture And Alligation: Explained With Selected Question & Answer

- Boats And Streams: Formula, Top Question With Solution (Aptitude)

- Clock Questions: Selected Question & Answer (Aptitude) Explained

Login to continue reading

And access exclusive content, personalized recommendations, and career-boosting opportunities.

Don't have an account? Sign up

Never miss an

Update

Featured Opportunities

Top-Rated Practice by Students

Subscribe

to our newsletter

Comments

Add comment